Sony and Beats Dominate Premium Segment with 54% Market Share by Value, While Soundcore Leads Volume with 8.2% Amidst Intense Low-Cost Competition

In the dynamic and highly competitive headphones market, characterized by rapid technological innovation and shifting consumer preferences, a nuanced understanding of brand positioning is paramount for strategic decision-making. The proliferation of e-commerce, accelerated by macroeconomic factors and changes in consumer behavior, has made marketplaces the primary battleground for market share. This analysis leverages granular data to dissect the competitive landscape, providing actionable insights into pricing strategies, consumer perception, and sales performance. The focus on a specific delivery ZIP code, 60007, provides a precise snapshot of local availability, logistics costs, and regional competitive intensity, offering a microcosm of broader national trends.

Methodology

This analysis is based on data aggregated by IndexBox's proprietary monitoring tools, which track product listings, pricing, sales volume, and customer reviews on the Amazon marketplace in the United States. The dataset was filtered for the product category 'Headphones' with delivery to ZIP code 60007, ensuring a consistent and geographically relevant view of availability and logistics. The data reflects real-time market conditions and is structured to analyze key performance indicators across major brands. For a comprehensive view of brand performance metrics, the data can be explored further on the IndexBox platform: IndexBox Brands Dashboard for Headphones.

Rating vs Reviews: Mapping Brand Perception and Engagement

The scatter plot reveals four distinct brand archetypes based on the median rating of 4.18 and median review count of 118.7. The 'Star Brands' quadrant, characterized by high ratings and high review volumes, includes Audio-Technica, Sony, and Beats. This indicates strong market presence, high customer satisfaction, and effective conversion of sales into social proof. 'Rising Brands' like Sennheiser and JVC have high review counts but slightly lower ratings, suggesting strong market penetration but potential issues with product consistency or customer expectations that require immediate attention to negative feedback. 'Niche Brands' such as Linsoul and JBL achieve high ratings but with fewer reviews, pointing to a loyal but smaller customer base and an opportunity to amplify marketing to drive volume. Finally, 'Problematic Brands' like Plantronics, Jabra, and Monster suffer from both lower ratings and fewer reviews, indicating a critical need for product quality reassessment and aggressive reputation management. Over time, brands can migrate between quadrants; for instance, a Rising Brand that systematically addresses negative feedback can become a Star, while a Star that neglects quality control can quickly become Problematic. Marketing levers must be tailored: Stars should focus on loyalty programs and leveraging UGC; Rising brands require proactive customer service and product iterations; Niche players need targeted advertising and influencer partnerships; Problematic brands must initiate deep product reviews and potentially disruptive promotions to regain visibility.

Price vs Sales Volume: Decoding Pricing Strategy Effectiveness

The analysis of average price against sales volume, with dot size representing the number of offers, uncovers clear strategic clusters. The 'Low Price / High Volume' quadrant is dominated by brands like MUSICOZY, JBL, and Soundcore, demonstrating high elasticity of demand and a volume-driven strategy that thrives on a wide assortment (evidenced by larger dots). Conversely, the 'High Price / High Volume' quadrant is sparsely populated, with only Sennheiser and Sony successfully commanding premium prices while maintaining significant sales volume, indicating strong brand equity and inelastic demand within their segments. Brands like Audio-Technica, Plantronics, and Jabra reside in the 'High Price / Low Volume' space, representing a premium niche strategy with higher margins but limited market reach, risking cannibalization if their assortment is not carefully curated. Linsoul and JVC in the 'Low Price / Low Volume' quadrant are in a challenging position, competing on price without achieving the sales scale of volume leaders. The data suggests an optimal strategy involves either dominating the volume game with a broad, low-cost assortment or building a defensible premium niche with a focused, high-margin offering. Attempting to straddle both often results in suboptimal performance.

Price Distribution: Identifying Market Sweet Spots and Anomalies

The histogram with Kernel Density Estimation (KDE) shows a highly right-skewed price distribution for headphones, with the vast majority of products clustered below the $150 mark. The density peaks sharply in the sub-$50 range, indicating intense competition and a mass-market focus. A secondary, smaller peak appears around the $200-$250 range, aligning with the successful premium strategies of Sony and Sennheiser. The long tail extending beyond $500 represents ultra-premium and specialist products, but the low density suggests a limited addressable market. The 'sweet spot' for mass-market volume is clearly under $100, while a profitable premium segment exists between $150 and $300. Anomalies in the extreme high-end (>$750) could indicate limited edition products, grey imports, or bundled offerings, but also present a risk of consumer distrust if pricing is not justified by perceived value. Assortment segmentation should be clear: budget-tier (<$50), mid-tier ($50-$150), premium ($150-$350), and specialist (>$350). Brands should test price elasticity within their segment; a hypothetical ±10% price change in the crowded budget tier could significantly impact volume, whereas a similar change in the premium tier may have a more muted effect on sales but a greater impact on margin.

Market Share by Sales Volume: Leadership and Portfolio Dynamics

The pie chart illustrates a fragmented market where the top 10 brands collectively command just over 50% of the sales volume, leaving a significant 40.3% share to the 'Others' category. Soundcore leads with 8.2%, followed by TOZO (6.7%) and JBL (6.3%), highlighting the strength of volume-oriented brands. This distribution underscores the challenge of achieving dominance and the opportunity within the long tail. For leaders like Soundcore, the strategy must focus on defending share through innovation, brand building, and portfolio diversification to cover multiple price points. For challengers in the top 10, targeted attacks on specific product segments or customer demographics are key. The large 'Others' segment is a critical battlefield; a deeper breakdown would likely reveal emerging brands and private labels that are collectively eroding share from established players. Investment in marketing and sales support for hero products within a portfolio is essential to break into the top ranks. The dynamics suggest that gains are often made at the expense of other players in the 'Others' basket rather than直接从 the absolute leader, making it a key area for strategic focus.

Price Distribution by Brand: Assessing Assortment Coherence and Competition

The boxplot analysis of selected brands reveals starkly different assortment and pricing strategies. MUSICOZY exhibits a very tight interquartile range (IQR) between $41 and $73, indicating a focused, low-cost strategy with minimal variability. In contrast, Linsoul and Audio-Technica show extremely wide IQRs and numerous high-value outliers, signaling a broad portfolio that spans from budget-friendly options to ultra-premium, specialist products exceeding $2000. This approach targets multiple segments but risks brand dilution and internal cannibalization. Plantronics also shows a wide range but with a higher median price, positioning it in the mid-to-premium market. JVC's distribution is concentrated at the lower end, similar to MUSICOZY. The significant overlap in the price ranges of these brands, particularly in the $50-$150 zone, indicates fierce competition and a high risk of price wars. Strategic recommendations include optimizing ranges to minimize overlap: brands like Audio-Technica should consider sub-branding for their premium outliers to protect the core brand equity, while volume players like MUSICOZY should continue to dominate their narrow price band with operational excellence.

Custom Search Request: Leveraging On-Demand Intelligence

The IndexBox platform's 'Custom Search Request' panel empowers users to move beyond static reports and conduct targeted, on-demand analysis. For instance, a marketing director can configure an API-driven alert to monitor real-time price changes and promotional campaigns for a specific set of competitor SKUs. This automation enables rapid response to competitive moves, such as launching a counter-promotion within hours. Another use case involves parsing customer reviews for newly launched products to gauge initial sentiment and identify potential quality issues before they escalate. This functionality can be integrated directly into Business Intelligence (BI) dashboards, providing a live feed of market data to inform daily decision-making across sales, marketing, and supply chain functions, transforming market intelligence from a periodic exercise into a continuous competitive advantage.

Conclusion

The headphone market is a tale of two strategies: volume-driven dominance in the low-cost segment and margin-focused leadership in the premium space. Success is contingent on a clear strategic alignment between price, product, and promotion, informed by a deep understanding of one's position within the competitive matrix. For investors, the opportunities lie in brands that have successfully carved out a defensible niche (either volume or premium) and demonstrate an ability to adapt. New entrants face significant barriers to entry, including established brand loyalty, economies of scale enjoyed by volume players, and the technical expertise required to compete in the premium audio segment. Continuous monitoring through platforms like IndexBox is not merely advantageous but essential for navigating this volatile and fast-paced market, allowing brands to anticipate shifts, capitalize on opportunities, and mitigate risks with precision and agility.

1. INTRODUCTION

Making Data-Driven Decisions to Grow Your Business

- REPORT DESCRIPTION

- RESEARCH METHODOLOGY AND THE AI PLATFORM

- DATA-DRIVEN DECISIONS FOR YOUR BUSINESS

- GLOSSARY AND SPECIFIC TERMS

2. EXECUTIVE SUMMARY

A Quick Overview of Market Performance

- KEY FINDINGS

- MARKET TRENDSThis Chapter is Available Only for the Professional EditionPRO

3. MARKET OVERVIEW

Understanding the Current State of The Market and its Prospects

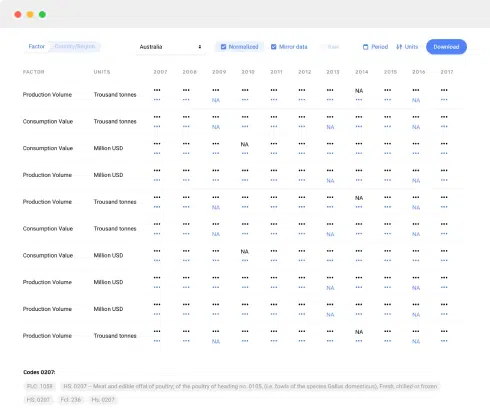

- MARKET SIZE: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- MARKET STRUCTURE: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- TRADE BALANCE: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- PER CAPITA CONSUMPTION: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- MARKET FORECAST TO 2035

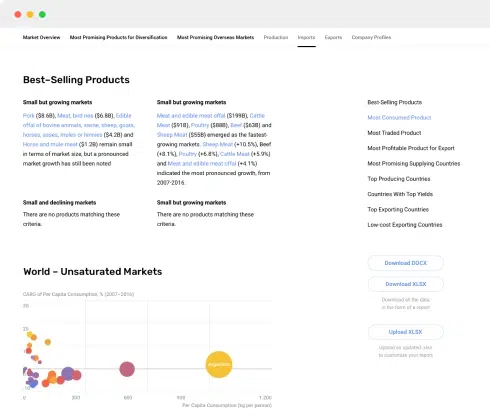

4. MOST PROMISING PRODUCTS FOR DIVERSIFICATION

Finding New Products to Diversify Your Business

- TOP PRODUCTS TO DIVERSIFY YOUR BUSINESS

- BEST-SELLING PRODUCTS

- MOST CONSUMED PRODUCTS

- MOST TRADED PRODUCTS

- MOST PROFITABLE PRODUCTS FOR EXPORTS

5. MOST PROMISING SUPPLYING COUNTRIES

Choosing the Best Countries to Establish Your Sustainable Supply Chain

- TOP COUNTRIES TO SOURCE YOUR PRODUCT

- TOP PRODUCING COUNTRIES

- TOP EXPORTING COUNTRIES

- LOW-COST EXPORTING COUNTRIES

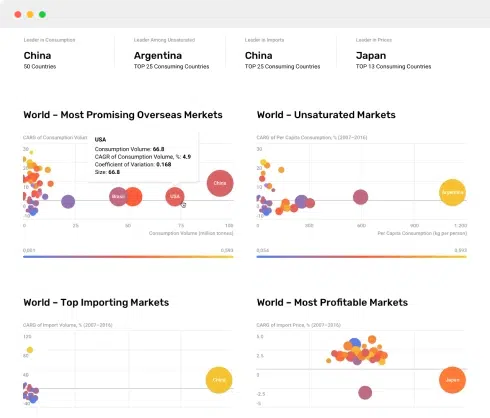

6. MOST PROMISING OVERSEAS MARKETS

Choosing the Best Countries to Boost Your Export

- TOP OVERSEAS MARKETS FOR EXPORTING YOUR PRODUCT

- TOP CONSUMING MARKETS

- UNSATURATED MARKETS

- TOP IMPORTING MARKETS

- MOST PROFITABLE MARKETS

7. PRODUCTION

The Latest Trends and Insights into The Industry

- PRODUCTION VOLUME AND VALUE: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

8. IMPORTS

The Largest Import Supplying Countries

- IMPORTS: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- IMPORTS BY COUNTRY: HISTORICAL DATA (2012–2024)

- IMPORT PRICES BY COUNTRY: HISTORICAL DATA (2012–2024)

9. EXPORTS

The Largest Destinations for Exports

- EXPORTS: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- EXPORTS BY COUNTRY: HISTORICAL DATA (2012–2024)

- EXPORT PRICES BY COUNTRY: HISTORICAL DATA (2012–2024)

10. PROFILES OF MAJOR PRODUCERS

The Largest Producers on The Market and Their Profiles

LIST OF TABLES

- Key Findings In 2024

- Market Volume, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Market Value: Historical Data (2012–2024) and Forecast (2025–2035)

- Per Capita Consumption: Historical Data (2012–2024) and Forecast (2025–2035)

- Imports, In Physical Terms, By Country, 2012–2024

- Imports, In Value Terms, By Country, 2012–2024

- Import Prices, By Country, 2012–2024

- Exports, In Physical Terms, By Country, 2012–2024

- Exports, In Value Terms, By Country, 2012–2024

- Export Prices, By Country, 2012–2024

LIST OF FIGURES

- Market Volume, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Market Value: Historical Data (2012–2024) and Forecast (2025–2035)

- Market Structure – Domestic Supply vs. Imports, in Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Market Structure – Domestic Supply vs. Imports, in Value Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Trade Balance, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Trade Balance, In Value Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Per Capita Consumption: Historical Data (2012–2024) and Forecast (2025–2035)

- Market Volume Forecast to 2035

- Market Value Forecast to 2035

- Market Size and Growth, By Product

- Average Per Capita Consumption, By Product

- Exports and Growth, By Product

- Export Prices and Growth, By Product

- Production Volume and Growth

- Exports and Growth

- Export Prices and Growth

- Market Size and Growth

- Per Capita Consumption

- Imports and Growth

- Import Prices

- Production, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Production, In Value Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Imports, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Imports, In Value Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Imports, In Physical Terms, By Country, 2024

- Imports, In Physical Terms, By Country, 2012–2024

- Imports, In Value Terms, By Country, 2012–2024

- Import Prices, By Country, 2012–2024

- Exports, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Exports, In Value Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Exports, In Physical Terms, By Country, 2024

- Exports, In Physical Terms, By Country, 2012–2024

- Exports, In Value Terms, By Country, 2012–2024

- Export Prices, By Country, 2012–2024