Headphone Market Analysis: Sony and Beats Lead with High Ratings and Volume

Key Findings

- Star brands like Sony and Beats dominate with high ratings and significant review volumes, indicating strong market trust and product quality.

- Premium brands such as Sennheiser and Audio-Technica command high prices but face lower sales volumes, highlighting a niche, high-margin strategy.

- The market is highly price-sensitive, with a concentration of sales in the sub-$100 segment, led by volume players like Soundcore and TOZO.

- Significant price dispersion exists within brand portfolios, suggesting opportunities for range optimization and potential cannibalization risks.

- Market share is heavily consolidated among the top 10 brands, with the "Others" segment representing a long tail of smaller competitors.

Methodology

The findings in this report are derived from an analysis of publicly available e-commerce data on the Amazon marketplace in the United States, with ZIP code 60007 as the delivery location. The data is collected by product categories using the search keyword "Headphones". For a deeper dive into brand-level metrics, please refer to the corresponding Brands section of IndexBox.

Rating vs Reviews

Star Brands (High Rating/High Reviews)

Brands like Sony, Beats, and Audio-Technica reside in this quadrant, representing market leaders. They have successfully converted high sales volumes into positive social proof. Their strategy should focus on maintaining quality and leveraging loyalty programs to defend their position.

Rising Brands (Low Rating/High Reviews)

Sennheiser and JVC have high visibility but sub-par ratings, indicating potential product or expectation mismatches. They must urgently analyze negative feedback for product improvements and actively manage their review responses to improve perceived quality.

Niche Brands (High Rating/Low Reviews)

Linsoul and JBL excel in quality but lack market awareness. Their marketing should focus on targeted influencer campaigns and sampling to drive review volume and transition into the Star quadrant.

Problematic Brands (Low Rating/Low Reviews)

Plantronics, Jabra, and Monster face challenges on both fronts. A comprehensive strategy is needed, involving product reevaluation, aggressive promotions to stimulate trials, and a revamped digital marketing approach to generate buzz.

Price vs Sales Volume

Volume-Driven Strategy

Brands like Soundcore and JBL operate with a low-price, high-volume model, indicating high price elasticity of demand. Their success is driven by maximizing market penetration and competing on value, requiring efficient logistics and mass-market advertising.

Premium Strategy

Sennheiser and Sony demonstrate that a high-price, high-volume position is achievable, targeting quality-conscious consumers. This suggests a relatively inelastic demand for trusted premium brands, allowing for strong margins alongside significant sales.

Niche Premium & Stagnant Segments

Audio-Technica and Plantronics occupy the high-price, low-volume quadrant, serving a specialized audience. Conversely, Linsoul and JVC in the low-price, low-volume segment risk obscurity and must either drive volume through marketing or justify a price increase.

Price Distribution

Market Sweet Spot

The distribution is heavily right-skewed, with a significant concentration of products and probability density below $100. This price band represents the core market "sweet spot" where competition is most intense and volume is highest.

Strategic Implications

Brands should segment their assortment to target specific price tiers: value (<$50), mainstream ($50-$150), and premium (>$150). Testing price changes within ±10% in the mainstream tier could optimize revenue without significantly impacting volume.

Anomaly Detection

The long tail of prices extending beyond $300 requires scrutiny. While some are justified by premium products, outliers could indicate grey market imports or counterfeits, necessitating brand protection measures.

Market Share

Market Concentration

The market is oligopolistic, with the top 10 brands commanding a significant majority of sales volume. Soundcore leads, indicating a successful value-oriented strategy that has captured a large consumer base.

Strategic Moves for Leaders

Leading brands should focus on portfolio diversification to cover multiple price segments and defend against challengers. They must also invest in brand building to reduce reliance on price competition.

The "Others" Segment

The "Others" category represents a long tail of smaller brands and is a source of disruption. Leaders should monitor this segment for emerging trends and consider acquisition targets among its top hidden players.

Boxplot Analysis

Assortment Width Analysis

Brands exhibit vastly different price range strategies. MUSICOZY has a very tight, low-price range, while Linsoul and Audio-Technica have extremely wide ranges, indicating a broad portfolio from entry-level to ultra-premium products.

Optimization Recommendations

Brands with wide ranges must analyze product performance to avoid cannibalization. Introducing clearer sub-brands or product lines for different tiers can help consumers navigate the assortment and justify price points.

Outlier Management

The high-value outliers for brands like Audio-Technica likely represent specialized professional equipment or limited editions. These products enhance brand prestige but should be marketed separately from the core consumer lineup.

Custom Search Request

On-Demand Competitive Intelligence

IndexBox allows for on-demand parsing through the "Custom Search Request" panel. A marketing director can automate this via API to continuously monitor competitor promotions, price changes, and new product launches, feeding real-time data into a BI dashboard for swift strategic response.

Conclusion

The headphone market is bifurcated into volume-driven and premium segments, with leadership requiring excellence in either operational efficiency or brand prestige. The analysis for ZIP 60007 reflects a typical suburban market with strong logistics and full product availability, making it a reliable proxy for national trends. Investors should focus on brands with a clear strategic position and a path to growth either in volume or margin. New entrants face high barriers to entry due to brand consolidation and must identify uncontested niche spaces. Regular monitoring through the IndexBox platform is recommended to track brand momentum and market shifts dynamically.

1. INTRODUCTION

Making Data-Driven Decisions to Grow Your Business

- REPORT DESCRIPTION

- RESEARCH METHODOLOGY AND THE AI PLATFORM

- DATA-DRIVEN DECISIONS FOR YOUR BUSINESS

- GLOSSARY AND SPECIFIC TERMS

2. EXECUTIVE SUMMARY

A Quick Overview of Market Performance

- KEY FINDINGS

- MARKET TRENDSThis Chapter is Available Only for the Professional EditionPRO

3. MARKET OVERVIEW

Understanding the Current State of The Market and its Prospects

- MARKET SIZE: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- MARKET STRUCTURE: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- TRADE BALANCE: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- PER CAPITA CONSUMPTION: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- MARKET FORECAST TO 2035

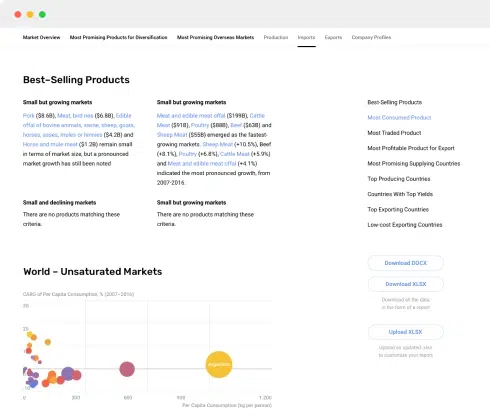

4. MOST PROMISING PRODUCTS FOR DIVERSIFICATION

Finding New Products to Diversify Your Business

- TOP PRODUCTS TO DIVERSIFY YOUR BUSINESS

- BEST-SELLING PRODUCTS

- MOST CONSUMED PRODUCTS

- MOST TRADED PRODUCTS

- MOST PROFITABLE PRODUCTS FOR EXPORTS

5. MOST PROMISING SUPPLYING COUNTRIES

Choosing the Best Countries to Establish Your Sustainable Supply Chain

- TOP COUNTRIES TO SOURCE YOUR PRODUCT

- TOP PRODUCING COUNTRIES

- TOP EXPORTING COUNTRIES

- LOW-COST EXPORTING COUNTRIES

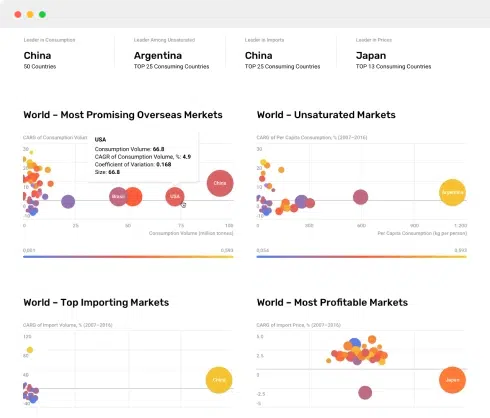

6. MOST PROMISING OVERSEAS MARKETS

Choosing the Best Countries to Boost Your Export

- TOP OVERSEAS MARKETS FOR EXPORTING YOUR PRODUCT

- TOP CONSUMING MARKETS

- UNSATURATED MARKETS

- TOP IMPORTING MARKETS

- MOST PROFITABLE MARKETS

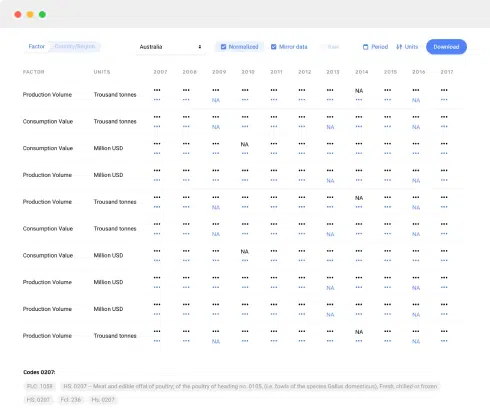

7. PRODUCTION

The Latest Trends and Insights into The Industry

- PRODUCTION VOLUME AND VALUE: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

8. IMPORTS

The Largest Import Supplying Countries

- IMPORTS: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- IMPORTS BY COUNTRY: HISTORICAL DATA (2012–2024)

- IMPORT PRICES BY COUNTRY: HISTORICAL DATA (2012–2024)

9. EXPORTS

The Largest Destinations for Exports

- EXPORTS: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- EXPORTS BY COUNTRY: HISTORICAL DATA (2012–2024)

- EXPORT PRICES BY COUNTRY: HISTORICAL DATA (2012–2024)

10. PROFILES OF MAJOR PRODUCERS

The Largest Producers on The Market and Their Profiles

LIST OF TABLES

- Key Findings In 2024

- Market Volume, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Market Value: Historical Data (2012–2024) and Forecast (2025–2035)

- Per Capita Consumption: Historical Data (2012–2024) and Forecast (2025–2035)

- Imports, In Physical Terms, By Country, 2012–2024

- Imports, In Value Terms, By Country, 2012–2024

- Import Prices, By Country, 2012–2024

- Exports, In Physical Terms, By Country, 2012–2024

- Exports, In Value Terms, By Country, 2012–2024

- Export Prices, By Country, 2012–2024

LIST OF FIGURES

- Market Volume, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Market Value: Historical Data (2012–2024) and Forecast (2025–2035)

- Market Structure – Domestic Supply vs. Imports, in Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Market Structure – Domestic Supply vs. Imports, in Value Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Trade Balance, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Trade Balance, In Value Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Per Capita Consumption: Historical Data (2012–2024) and Forecast (2025–2035)

- Market Volume Forecast to 2035

- Market Value Forecast to 2035

- Market Size and Growth, By Product

- Average Per Capita Consumption, By Product

- Exports and Growth, By Product

- Export Prices and Growth, By Product

- Production Volume and Growth

- Exports and Growth

- Export Prices and Growth

- Market Size and Growth

- Per Capita Consumption

- Imports and Growth

- Import Prices

- Production, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Production, In Value Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Imports, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Imports, In Value Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Imports, In Physical Terms, By Country, 2024

- Imports, In Physical Terms, By Country, 2012–2024

- Imports, In Value Terms, By Country, 2012–2024

- Import Prices, By Country, 2012–2024

- Exports, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Exports, In Value Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Exports, In Physical Terms, By Country, 2024

- Exports, In Physical Terms, By Country, 2012–2024

- Exports, In Value Terms, By Country, 2012–2024

- Export Prices, By Country, 2012–2024