Headphone Market Analysis: Sony & Beats Lead as Star Brands with High Ratings and Volume

Key Findings

- Market leadership is concentrated among brands like Soundcore and JBL, which successfully combine high volume with competitive pricing.

- A clear segmentation exists between premium brands (e.g., Sennheiser, Audio-Technica) focusing on high-margin niches and value brands (e.g., MUSICOZY) competing on volume.

- The price distribution is heavily right-skewed, indicating a long tail of premium products alongside a dense concentration of offerings under $100.

- Brands demonstrate varied strategic positions in the rating-reviews matrix, with Sony and Beats achieving the ideal "Star" quadrant of high ratings and high review volume.

- Significant price dispersion within individual brand portfolios suggests sophisticated multi-tier product strategies but also potential for internal cannibalization.

Methodology

The findings in this report are derived from an analysis of publicly available e-commerce data on the Amazon marketplace in the United States, with ZIP code 60007 as the delivery location. The data is collected by product categories using the search keyword "Headphones". For a deeper dive into brand-level metrics, access the full dataset via the IndexBox Brands section.

Rating vs Reviews

Star Brands (High Rating/High Reviews): Sony, Beats, and Audio-Technica represent the ideal position, indicating strong market acceptance and product quality. To maintain their leadership, these brands should focus on defending their premium positioning through innovation and leveraging positive social proof in marketing campaigns.

Rising Brands (Low Rating/High Reviews): Sennheiser and JVC have significant market reach but subpar ratings, suggesting potential issues with product-market fit or customer expectations. Immediate action should include a deep analysis of negative feedback to guide product improvements and a proactive customer service strategy to address public complaints.

Niche Brands (High Rating/Low Reviews): Linsoul and JBL produce high-quality products but lack market awareness. Their strategy should pivot towards amplified marketing efforts, including influencer partnerships and targeted advertising, to convert their excellent user satisfaction into greater market share.

Problematic Brands (Low Rating/Low Reviews): Plantronics, Jabra, and Monster are challenged on both perception and visibility. A fundamental reassessment of product quality is required, coupled with aggressive promotional tactics to generate initial sales volume and fresh reviews to reset their brand narrative.

Price vs Sales Volume

Premium Strategy Analysis: Sennheiser and Sony successfully operate in the high-price, high-volume quadrant, demonstrating inelastic demand for trusted premium brands. Their focus should remain on innovation and brand equity to justify their price points and avoid discount-driven erosion of perceived value.

Value Strategy Analysis: Brands like MUSICOZY and Soundcore dominate the low-price, high-volume quadrant, indicating highly elastic demand. They compete on efficiency and scale; their key lever is optimizing supply chain and customer acquisition costs to protect thin margins.

Portfolio Optimization: Brands in the high-price, low-volume quadrant (e.g., Audio-Technica) occupy a profitable niche but should explore sub-brands or limited-time offers to attract a broader audience without diluting their core premium identity. The large number of offers for some brands risks cannibalization and requires careful portfolio management.

Price Distribution

Market Segmentation: The distribution is strongly right-skewed, with a pronounced concentration of products below $100, indicating a mass-market, price-sensitive segment. A second, smaller peak appears in the $200-$250 range, representing a established premium segment for audiophiles and professionals.

Strategic Recommendations: The "sweet spot" for mass-market volume lies between $50-$120. Brands should test price increases within this band cautiously, as demand is likely elastic. For premium offerings, value-based pricing is more effective than cost-plus, focusing on superior features and brand storytelling to justify the premium.

Anomaly Detection: The long tail of prices exceeding $500 requires scrutiny for potential grey market imports or counterfeit products, which can damage brand reputation. Authentic ultra-premium products should be clearly differentiated through certified storefronts and unique serial numbers.

Market Share

Market Concentration: The market is semi-fragmented, with the top 10 brands holding a significant share but the "Others" category representing a substantial 30% of volume. This indicates a long tail of smaller players and private labels successfully competing on niche use-cases or hyper-low prices.

Strategic Moves for Leaders: Leading brands must defend share through continuous innovation and marketing spend while considering strategic acquisitions of emerging players in the "Others" category to acquire customers and technology. Portfolio diversification into adjacent categories (e.g., gaming headsets) can drive new growth.

Opportunities for Challengers: For brands in the "Others" segment, the strategy should be one of focus. Identifying and dominating a specific sub-segment (e.g., sleep headphones, kids' headphones) is more viable than competing broadly with the marketing budgets of the top players.

Boxplot Analysis

Assortment Width Analysis: Brands like Linsoul and Audio-Technica show extreme price dispersion, indicating a very wide assortment from entry-level to ultra-premium products. This strategy targets multiple consumer segments but carries a high risk of brand dilution and internal cannibalization if not managed carefully.

Optimizing Price Ranges: Brands with narrow boxes (e.g., MUSICOZY) have a focused positioning. Brands with wide boxes should consider creating clearer sub-brand architectures to logically segment their offerings and justify the vast price differences to consumers, thus minimizing confusion.

Outlier Management: The high-value outliers for brands like Audio-Technica likely represent limited edition or professional-grade equipment. These products should be marketed as halo products to enhance brand prestige, rather than being expected to generate significant volume, and their pricing should remain aspirational.

Custom Search Request

The IndexBox platform allows for on-demand parsing through its "Custom Search Request" panel. A marketing director can automate this function via API to continuously monitor competitor promotions, price changes, and new product launches. This real-time competitive intelligence can be integrated directly into BI dashboards, enabling data-driven decision-making for dynamic pricing and promotional strategy adjustments without manual effort.

Conclusion

Summary of Insights: The headphone market is a bifurcated landscape, split between volume-driven value players and margin-focused premium brands. Success is contingent on a clear strategic positioning within one of these paradigms, supported by a product portfolio and marketing strategy that consistently reinforces that position.

Regional Perspective: Analysis for ZIP 60007 confirms nationwide availability for major brands but may slightly inflate the visibility of brands with strong distribution partnerships with Amazon or local retailers. Logistics in this region are efficient, minimizing delivery times as a significant competitive factor.

Strategic Recommendations: Investors should focus on brands with a defensible position in either the high-volume or high-margin quadrants. Barriers to entry are high due to established brand loyalty and the required marketing investment; new players must identify an uncontested niche or disruptive business model to succeed. We recommend regular monitoring of these dynamics through the IndexBox platform to stay ahead of market shifts.

1. INTRODUCTION

Making Data-Driven Decisions to Grow Your Business

- REPORT DESCRIPTION

- RESEARCH METHODOLOGY AND THE AI PLATFORM

- DATA-DRIVEN DECISIONS FOR YOUR BUSINESS

- GLOSSARY AND SPECIFIC TERMS

2. EXECUTIVE SUMMARY

A Quick Overview of Market Performance

- KEY FINDINGS

- MARKET TRENDSThis Chapter is Available Only for the Professional EditionPRO

3. MARKET OVERVIEW

Understanding the Current State of The Market and its Prospects

- MARKET SIZE: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- MARKET STRUCTURE: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- TRADE BALANCE: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- PER CAPITA CONSUMPTION: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- MARKET FORECAST TO 2035

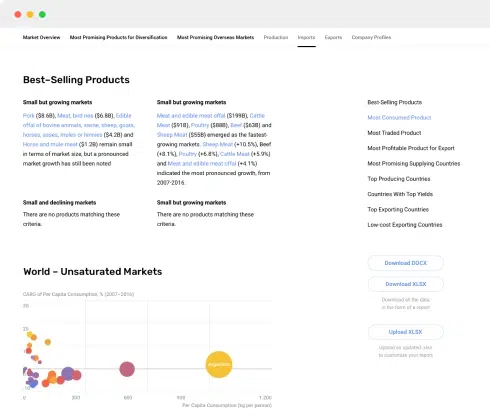

4. MOST PROMISING PRODUCTS FOR DIVERSIFICATION

Finding New Products to Diversify Your Business

- TOP PRODUCTS TO DIVERSIFY YOUR BUSINESS

- BEST-SELLING PRODUCTS

- MOST CONSUMED PRODUCTS

- MOST TRADED PRODUCTS

- MOST PROFITABLE PRODUCTS FOR EXPORTS

5. MOST PROMISING SUPPLYING COUNTRIES

Choosing the Best Countries to Establish Your Sustainable Supply Chain

- TOP COUNTRIES TO SOURCE YOUR PRODUCT

- TOP PRODUCING COUNTRIES

- TOP EXPORTING COUNTRIES

- LOW-COST EXPORTING COUNTRIES

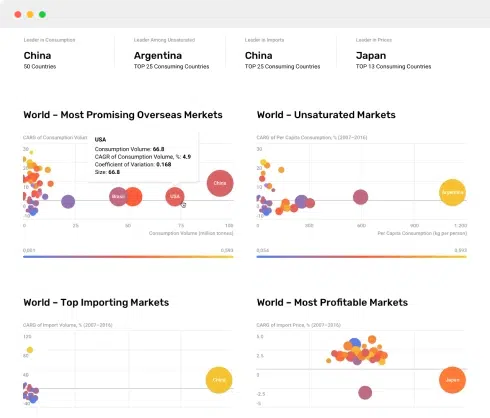

6. MOST PROMISING OVERSEAS MARKETS

Choosing the Best Countries to Boost Your Export

- TOP OVERSEAS MARKETS FOR EXPORTING YOUR PRODUCT

- TOP CONSUMING MARKETS

- UNSATURATED MARKETS

- TOP IMPORTING MARKETS

- MOST PROFITABLE MARKETS

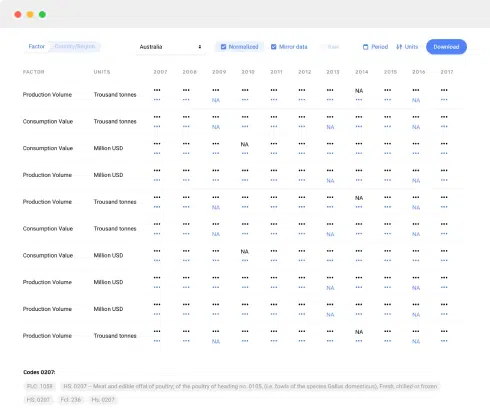

7. PRODUCTION

The Latest Trends and Insights into The Industry

- PRODUCTION VOLUME AND VALUE: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

8. IMPORTS

The Largest Import Supplying Countries

- IMPORTS: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- IMPORTS BY COUNTRY: HISTORICAL DATA (2012–2024)

- IMPORT PRICES BY COUNTRY: HISTORICAL DATA (2012–2024)

9. EXPORTS

The Largest Destinations for Exports

- EXPORTS: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- EXPORTS BY COUNTRY: HISTORICAL DATA (2012–2024)

- EXPORT PRICES BY COUNTRY: HISTORICAL DATA (2012–2024)

10. PROFILES OF MAJOR PRODUCERS

The Largest Producers on The Market and Their Profiles

LIST OF TABLES

- Key Findings In 2024

- Market Volume, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Market Value: Historical Data (2012–2024) and Forecast (2025–2035)

- Per Capita Consumption: Historical Data (2012–2024) and Forecast (2025–2035)

- Imports, In Physical Terms, By Country, 2012–2024

- Imports, In Value Terms, By Country, 2012–2024

- Import Prices, By Country, 2012–2024

- Exports, In Physical Terms, By Country, 2012–2024

- Exports, In Value Terms, By Country, 2012–2024

- Export Prices, By Country, 2012–2024

LIST OF FIGURES

- Market Volume, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Market Value: Historical Data (2012–2024) and Forecast (2025–2035)

- Market Structure – Domestic Supply vs. Imports, in Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Market Structure – Domestic Supply vs. Imports, in Value Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Trade Balance, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Trade Balance, In Value Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Per Capita Consumption: Historical Data (2012–2024) and Forecast (2025–2035)

- Market Volume Forecast to 2035

- Market Value Forecast to 2035

- Market Size and Growth, By Product

- Average Per Capita Consumption, By Product

- Exports and Growth, By Product

- Export Prices and Growth, By Product

- Production Volume and Growth

- Exports and Growth

- Export Prices and Growth

- Market Size and Growth

- Per Capita Consumption

- Imports and Growth

- Import Prices

- Production, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Production, In Value Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Imports, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Imports, In Value Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Imports, In Physical Terms, By Country, 2024

- Imports, In Physical Terms, By Country, 2012–2024

- Imports, In Value Terms, By Country, 2012–2024

- Import Prices, By Country, 2012–2024

- Exports, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Exports, In Value Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Exports, In Physical Terms, By Country, 2024

- Exports, In Physical Terms, By Country, 2012–2024

- Exports, In Value Terms, By Country, 2012–2024

- Export Prices, By Country, 2012–2024