Headphone Market Analysis: Sony and Beats Lead with High Ratings and Volume

Key Findings

- Star brands like Sony and Beats demonstrate a strong product-market fit with high ratings and significant review volumes, indicating robust brand equity.

- The market exhibits a clear segmentation between low-cost, high-volume players (e.g., Soundcore) and premium, lower-volume specialists (e.g., Audio-Technica), suggesting distinct consumer purchasing drivers.

- Price distribution is heavily right-skewed, with a concentration of offers below $150, highlighting a highly competitive mass market and a long-tail of premium products.

- Market share by volume is fragmented, with the top 10 brands holding a combined share of approximately 55%, while the "Others" category represents a significant 45% of the market.

- Significant price dispersion exists within individual brand portfolios, indicating diverse product lines that cater to different consumer segments and price points.

Methodology

The findings in this report are derived from an analysis of publicly available e-commerce data on the Amazon marketplace in the United States, with ZIP code 60007 as the delivery location. The data is collected by product categories using the search keyword "Headphones" and is accessible for further exploration via the Brands section of IndexBox. This specific ZIP code, representing a suburban area near Chicago, can influence product availability and shipping logistics, potentially favoring Fulfillment by Amazon (FBA) sellers.

Rating vs Reviews

Star Brands Audio-Technica, Sony, and Beats occupy the coveted high-rating, high-reviews quadrant. This indicates strong customer satisfaction and high market penetration. To maintain this position, focus on innovation and leveraging positive social proof in marketing campaigns.

Rising Brands Sennheiser and JVC have high review counts but slightly lower ratings, suggesting high visibility with some quality or expectation mismatches. The priority is to analyze negative feedback to improve product quality and actively manage customer reviews to boost ratings.

Niche Brands Linsoul and JBL achieve high ratings but have a smaller review base, indicating excellent quality for a dedicated audience. They should focus on targeted marketing to increase awareness and conversion, potentially using influencer partnerships within their specific niche.

Problematic Brands Plantronics, Jabra, and Monster suffer from lower ratings and fewer reviews, indicating limited market impact and potential product issues. A fundamental product reassessment is needed, coupled with aggressive promotional strategies to generate initial sales and reviews.

Price vs Sales Volume

Premium Strategy Sennheiser and Sony successfully operate in the high-price, high-volume quadrant, demonstrating inelastic demand and strong brand power. They should continue to innovate and justify their premium positioning through superior technology and brand storytelling.

Value Strategy Brands like JBL, Soundcore, and MUSICOZY dominate the low-price, high-volume space, indicating highly elastic demand. Their focus should be on supply chain optimization and economies of scale to protect margins while maintaining aggressive pricing.

Niche Premium Audio-Technica, Plantronics, and Jabra are high-price with low volume, serving specialized segments. They must clearly communicate their unique value proposition to justify the price and avoid cannibalization by expanding into adjacent, more mainstream price points cautiously.

Low Engagement Linsoul and JVC sit in the low-price, low-volume quadrant, indicating a lack of clear market positioning. They need to reassess their target audience and differentiate through features or marketing to drive volume.

Price Distribution

Market Concentration The histogram shows a strong right skew, with the vast majority of products priced under $150. The Kernel Density Estimate (KDE) confirms the highest density is below $100, identifying the core competitive battleground.

Strategic Sweet Spots The data suggests key price points at sub-$50 (ultra-budget), $50-$100 (value mainstream), and $150-$250 (premium mainstream). Brands should align their portfolios to target these specific consumer expectation brackets.

Anomaly Detection The long tail of products priced above $300 requires scrutiny. While some are legitimate high-end products, this range can also be susceptible to grey market imports or pricing errors, necessitating vigilant monitoring.

Market Share

Market Fragmentation The market is fragmented, with the "Others" category holding a 45% share. This indicates a long tail of small brands and white-label products, presenting both a threat to incumbents and an opportunity for acquisition or partnership.

Leadership Defense Volume leaders like Soundcore and JBL must defend their position through continuous innovation and marketing spend efficiency. They should explore sub-brands to attack different price segments without diluting the master brand.

Portfolio Diversification For brands in the middle of the ranking, diversification is key. They should analyze the "Others" segment to identify emerging trends and potential acquisition targets to consolidate their market position.

Boxplot

Assortment Width Brands exhibit vastly different price range strategies. Linsoul and Audio-Technica have extremely wide interquartile ranges and high outliers, indicating a broad portfolio from mid-range to ultra-premium offerings, including limited editions.

Focused Positioning In contrast, MUSICOZY shows a very narrow price range, suggesting a focused value proposition. This minimizes internal cannibalization but also limits addressable market share.

Optimization Strategy Brands with wide ranges should analyze sales concentration within their portfolio. They may consider rationalizing SKUs at overlapping price points to reduce complexity and focus on bestsellers.

Custom Search Request

The IndexBox platform allows for on-demand data updates through its "Custom Search Request" panel. A marketing director can use this function to automatically monitor competitor promotions, tracking changes in price and availability for key SKUs in real-time. This data can be integrated directly into BI dashboards, enabling automated alerting and dynamic pricing strategies, transforming market intelligence from a periodic report into a live operational tool.

Conclusion

The headphone market is a complex landscape of volume-driven value brands and margin-focused premium players. Success requires a clear strategic positioning, whether through cost leadership or differentiated branding. Investors should focus on brands with a defensible niche or superior supply chain capabilities, while new entrants face significant barriers from established marketing ecosystems and volume-based logistics advantages. Continuous monitoring of these dynamic factors through platforms like IndexBox is not an option but a necessity for maintaining competitive advantage.

1. INTRODUCTION

Making Data-Driven Decisions to Grow Your Business

- REPORT DESCRIPTION

- RESEARCH METHODOLOGY AND THE AI PLATFORM

- DATA-DRIVEN DECISIONS FOR YOUR BUSINESS

- GLOSSARY AND SPECIFIC TERMS

2. EXECUTIVE SUMMARY

A Quick Overview of Market Performance

- KEY FINDINGS

- MARKET TRENDSThis Chapter is Available Only for the Professional EditionPRO

3. MARKET OVERVIEW

Understanding the Current State of The Market and its Prospects

- MARKET SIZE: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- MARKET STRUCTURE: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- TRADE BALANCE: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- PER CAPITA CONSUMPTION: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- MARKET FORECAST TO 2035

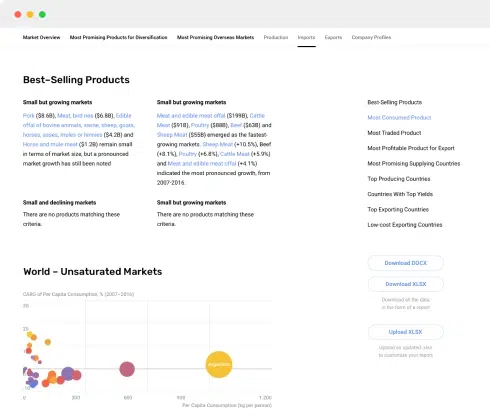

4. MOST PROMISING PRODUCTS FOR DIVERSIFICATION

Finding New Products to Diversify Your Business

- TOP PRODUCTS TO DIVERSIFY YOUR BUSINESS

- BEST-SELLING PRODUCTS

- MOST CONSUMED PRODUCTS

- MOST TRADED PRODUCTS

- MOST PROFITABLE PRODUCTS FOR EXPORTS

5. MOST PROMISING SUPPLYING COUNTRIES

Choosing the Best Countries to Establish Your Sustainable Supply Chain

- TOP COUNTRIES TO SOURCE YOUR PRODUCT

- TOP PRODUCING COUNTRIES

- TOP EXPORTING COUNTRIES

- LOW-COST EXPORTING COUNTRIES

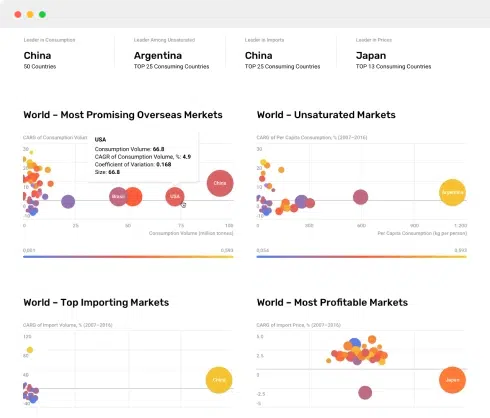

6. MOST PROMISING OVERSEAS MARKETS

Choosing the Best Countries to Boost Your Export

- TOP OVERSEAS MARKETS FOR EXPORTING YOUR PRODUCT

- TOP CONSUMING MARKETS

- UNSATURATED MARKETS

- TOP IMPORTING MARKETS

- MOST PROFITABLE MARKETS

7. PRODUCTION

The Latest Trends and Insights into The Industry

- PRODUCTION VOLUME AND VALUE: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

8. IMPORTS

The Largest Import Supplying Countries

- IMPORTS: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- IMPORTS BY COUNTRY: HISTORICAL DATA (2012–2024)

- IMPORT PRICES BY COUNTRY: HISTORICAL DATA (2012–2024)

9. EXPORTS

The Largest Destinations for Exports

- EXPORTS: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- EXPORTS BY COUNTRY: HISTORICAL DATA (2012–2024)

- EXPORT PRICES BY COUNTRY: HISTORICAL DATA (2012–2024)

10. PROFILES OF MAJOR PRODUCERS

The Largest Producers on The Market and Their Profiles

LIST OF TABLES

- Key Findings In 2024

- Market Volume, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Market Value: Historical Data (2012–2024) and Forecast (2025–2035)

- Per Capita Consumption: Historical Data (2012–2024) and Forecast (2025–2035)

- Imports, In Physical Terms, By Country, 2012–2024

- Imports, In Value Terms, By Country, 2012–2024

- Import Prices, By Country, 2012–2024

- Exports, In Physical Terms, By Country, 2012–2024

- Exports, In Value Terms, By Country, 2012–2024

- Export Prices, By Country, 2012–2024

LIST OF FIGURES

- Market Volume, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Market Value: Historical Data (2012–2024) and Forecast (2025–2035)

- Market Structure – Domestic Supply vs. Imports, in Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Market Structure – Domestic Supply vs. Imports, in Value Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Trade Balance, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Trade Balance, In Value Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Per Capita Consumption: Historical Data (2012–2024) and Forecast (2025–2035)

- Market Volume Forecast to 2035

- Market Value Forecast to 2035

- Market Size and Growth, By Product

- Average Per Capita Consumption, By Product

- Exports and Growth, By Product

- Export Prices and Growth, By Product

- Production Volume and Growth

- Exports and Growth

- Export Prices and Growth

- Market Size and Growth

- Per Capita Consumption

- Imports and Growth

- Import Prices

- Production, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Production, In Value Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Imports, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Imports, In Value Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Imports, In Physical Terms, By Country, 2024

- Imports, In Physical Terms, By Country, 2012–2024

- Imports, In Value Terms, By Country, 2012–2024

- Import Prices, By Country, 2012–2024

- Exports, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Exports, In Value Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Exports, In Physical Terms, By Country, 2024

- Exports, In Physical Terms, By Country, 2012–2024

- Exports, In Value Terms, By Country, 2012–2024

- Export Prices, By Country, 2012–2024