Headphone Market Analysis: Sony and Beats Lead with High Ratings and Volume

Key Findings

- The headphone market exhibits a competitive structure with a significant long tail, where the top 10 brands hold a combined share of approximately 60% of total sales volume, indicating opportunities for niche players.

- Brands are distinctly segmented by price and volume strategies, with clear leaders in the high-volume, low-price segment (e.g., Soundcore, JBL) and the high-volume, high-price segment (e.g., Sony, Sennheiser).

- Analysis of rating versus reviews reveals that brands like Sony and Beats achieve strong market penetration with high customer satisfaction, while others like Sennheiser show high engagement but room for quality improvement.

- Price distribution is heavily right-skewed, with the majority of products concentrated below $150, presenting a clear "sweet spot" for mass-market appeal, while premium niches exist above $200.

- Significant price variability within brand portfolios, as seen with Linsoul and Audio-Technica, suggests diversified targeting but also potential for internal cannibalization and price competition.

Methodology

The findings in this report are derived from an analysis of publicly available e-commerce data on the Amazon marketplace in the United States, with ZIP code 60007 as the delivery location. The data is collected by product categories using the search keyword "Headphones". For a dynamic and detailed view of brand performance, refer to the Brands section of IndexBox.

Chapter 1. Brand Analysis

Rating vs Reviews The scatter plot segments brands into four strategic quadrants based on median rating (4.181) and review count (118.748k). High Rating / High Reviews Star brands like Sony, Beats, and Audio-Technica combine strong market presence with high customer satisfaction. They should defend their position by leveraging social proof in marketing and continuing to invest in product quality and innovation. Low Rating / High Reviews Rising brands such as Sennheiser and JVC have achieved significant market penetration but face quality perception issues. Their immediate priority must be a rigorous analysis of negative feedback to address product flaws and improve customer service, converting their large user base into advocates. High Rating / Low Reviews Niche players like Linsoul and JBL are praised by a smaller, likely more expert, audience. They should focus on targeted influencer marketing and loyalty programs to amplify their positive word-of-mouth and drive consideration among a broader audience. Low Rating / Low Reviews Problematic brands including Plantronics, Jabra, and Monster are struggling with both visibility and satisfaction. A fundamental product reassessment is required, coupled with aggressive promotional tactics to generate initial sales volume and fresh reviews, potentially through limited-time discounts.

Price vs Sales Volume The analysis reveals distinct strategic positioning based on median price ($154.55) and sales volume (32.05k units). Low Price / High Volume Brands like Soundcore and JBL operate in a highly elastic demand environment, where volume is highly sensitive to price changes. Their strategy of competitive pricing and a wide number of offers (200-300 SKUs) is effective for mass-market dominance, but they must vigilantly manage margins and avoid cannibalization within their own portfolios. High Price / High Volume Sony and Sennheiser demonstrate that a premium positioning can also achieve high volume, indicating strong brand equity and perceived value. They should continue to justify their price points through superior technology, branding, and exclusive features, protecting themselves from low-cost competitors. High Price / Low Volume Audio-Technica, Jabra, and Plantronics occupy a high-margin, low-volume niche. Their focus should be on maximizing profitability per unit through exceptional quality and customer service, rather than competing on volume or price. Low Price / Low Volume Brands like JVC and Linsoul are in a challenging position with neither a price nor a volume advantage. They need to differentiate through unique product features, design, or targeting very specific use cases to escape this quadrant.

Market Shares by Sales Volume The market structure is competitive and fragmented, not monopolized. The top player, Soundcore, holds only an 11.6% share, and the combined "Others" segment represents a substantial 28.6% of the market. This significant long tail indicates a healthy ecosystem for niche brands to thrive by catering to specific consumer needs that leaders overlook. For leading brands, strategy must focus on defending share through innovation and marketing spend efficiency. For smaller brands and those in the "Others" category, the opportunity lies in hyper-specialization, targeting underserved segments, and leveraging agile marketing to chip away at the leaders' volume.

Chapter 2. Price analysis

Price Distribution The price distribution is strongly right-skewed, with a pronounced concentration of products (and probability density) below $150. The histogram and KDE curve identify the core market "sweet spot" between approximately $50 and $120. Pricing experiments within this range (±10-15%) are likely to have the most significant impact on volume and competitive positioning. The long tail of prices extending beyond $250 represents premium and specialist niches with inelastic demand; brands operating here compete on perceived value and exclusivity, not price. Anomalies at the very high end (>$500) could indicate limited editions, professional-grade equipment, or require scrutiny for potential grey market listings.

Boxplot The boxplot analysis reveals starkly different assortment and pricing strategies. MUSICOZY and JVC show tight, low-price ranges, indicating a focused, budget-oriented strategy. In contrast, Linsoul and Audio-Technica exhibit extremely wide interquartile ranges and numerous high-value outliers, signaling a broad portfolio that targets both entry-level and ultra-premium segments. This wide dispersion creates a risk of internal cannibalization and brand positioning confusion. For such brands, optimizing the assortment may involve rationalizing SKUs to reduce overlap and clarifying sub-brand architectures to distinctly segment offerings by price and feature sets, thereby minimizing internal competition.

Custom Search Request The IndexBox platform's "Custom Search Request" panel enables on-demand data parsing to answer specific strategic questions. For instance, a Marketing Director can automate a daily API call to monitor real-time price changes and promotional activities of key competitors like Sony and JBL. This data can be fed directly into a BI dashboard, triggering alerts for rapid response campaigns, making competitive intelligence gathering a continuous and automated process rather than a manual, periodic task.

Conclusion The headphone market is dynamic and segmented, offering pathways for both volume-driven and premium strategies. Success hinges on a clear understanding of one's position within the rating-reviews and price-volume matrices. Leaders must defend share through innovation, while challengers can exploit niches within the large "Others" segment. The ZIP code 60007 (a Chicago suburb) suggests a typical suburban demographic with standard logistics and availability, making the findings broadly representative of the U.S. mass market. For investors, the market offers opportunities in both scaling low-cost manufacturers and high-margin niche brands. New entrants face the primary barrier of establishing brand recognition and trust in a crowded field, where customer reviews and ratings are critical currencies. Regular monitoring of these dynamics through IndexBox is essential for maintaining a competitive edge.

1. INTRODUCTION

Making Data-Driven Decisions to Grow Your Business

- REPORT DESCRIPTION

- RESEARCH METHODOLOGY AND THE AI PLATFORM

- DATA-DRIVEN DECISIONS FOR YOUR BUSINESS

- GLOSSARY AND SPECIFIC TERMS

2. EXECUTIVE SUMMARY

A Quick Overview of Market Performance

- KEY FINDINGS

- MARKET TRENDSThis Chapter is Available Only for the Professional EditionPRO

3. MARKET OVERVIEW

Understanding the Current State of The Market and its Prospects

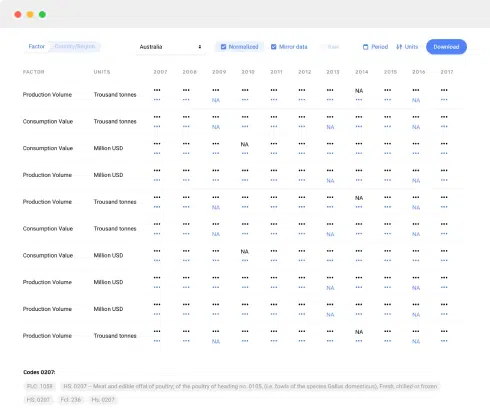

- MARKET SIZE: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- MARKET STRUCTURE: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- TRADE BALANCE: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- PER CAPITA CONSUMPTION: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- MARKET FORECAST TO 2035

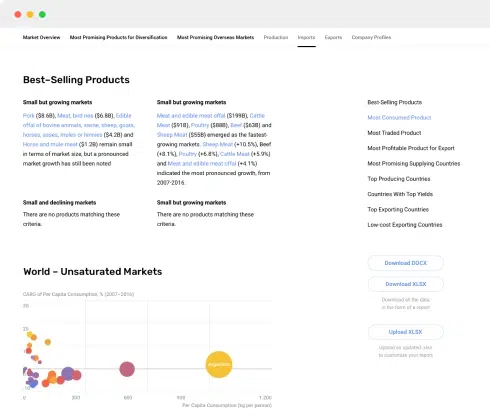

4. MOST PROMISING PRODUCTS FOR DIVERSIFICATION

Finding New Products to Diversify Your Business

- TOP PRODUCTS TO DIVERSIFY YOUR BUSINESS

- BEST-SELLING PRODUCTS

- MOST CONSUMED PRODUCTS

- MOST TRADED PRODUCTS

- MOST PROFITABLE PRODUCTS FOR EXPORTS

5. MOST PROMISING SUPPLYING COUNTRIES

Choosing the Best Countries to Establish Your Sustainable Supply Chain

- TOP COUNTRIES TO SOURCE YOUR PRODUCT

- TOP PRODUCING COUNTRIES

- TOP EXPORTING COUNTRIES

- LOW-COST EXPORTING COUNTRIES

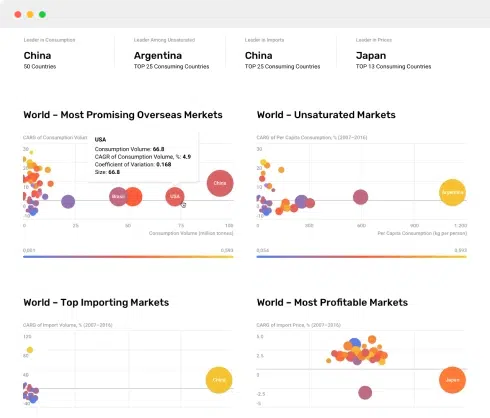

6. MOST PROMISING OVERSEAS MARKETS

Choosing the Best Countries to Boost Your Export

- TOP OVERSEAS MARKETS FOR EXPORTING YOUR PRODUCT

- TOP CONSUMING MARKETS

- UNSATURATED MARKETS

- TOP IMPORTING MARKETS

- MOST PROFITABLE MARKETS

7. PRODUCTION

The Latest Trends and Insights into The Industry

- PRODUCTION VOLUME AND VALUE: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

8. IMPORTS

The Largest Import Supplying Countries

- IMPORTS: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- IMPORTS BY COUNTRY: HISTORICAL DATA (2012–2024)

- IMPORT PRICES BY COUNTRY: HISTORICAL DATA (2012–2024)

9. EXPORTS

The Largest Destinations for Exports

- EXPORTS: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- EXPORTS BY COUNTRY: HISTORICAL DATA (2012–2024)

- EXPORT PRICES BY COUNTRY: HISTORICAL DATA (2012–2024)

10. PROFILES OF MAJOR PRODUCERS

The Largest Producers on The Market and Their Profiles

LIST OF TABLES

- Key Findings In 2024

- Market Volume, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Market Value: Historical Data (2012–2024) and Forecast (2025–2035)

- Per Capita Consumption: Historical Data (2012–2024) and Forecast (2025–2035)

- Imports, In Physical Terms, By Country, 2012–2024

- Imports, In Value Terms, By Country, 2012–2024

- Import Prices, By Country, 2012–2024

- Exports, In Physical Terms, By Country, 2012–2024

- Exports, In Value Terms, By Country, 2012–2024

- Export Prices, By Country, 2012–2024

LIST OF FIGURES

- Market Volume, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Market Value: Historical Data (2012–2024) and Forecast (2025–2035)

- Market Structure – Domestic Supply vs. Imports, in Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Market Structure – Domestic Supply vs. Imports, in Value Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Trade Balance, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Trade Balance, In Value Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Per Capita Consumption: Historical Data (2012–2024) and Forecast (2025–2035)

- Market Volume Forecast to 2035

- Market Value Forecast to 2035

- Market Size and Growth, By Product

- Average Per Capita Consumption, By Product

- Exports and Growth, By Product

- Export Prices and Growth, By Product

- Production Volume and Growth

- Exports and Growth

- Export Prices and Growth

- Market Size and Growth

- Per Capita Consumption

- Imports and Growth

- Import Prices

- Production, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Production, In Value Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Imports, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Imports, In Value Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Imports, In Physical Terms, By Country, 2024

- Imports, In Physical Terms, By Country, 2012–2024

- Imports, In Value Terms, By Country, 2012–2024

- Import Prices, By Country, 2012–2024

- Exports, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Exports, In Value Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Exports, In Physical Terms, By Country, 2024

- Exports, In Physical Terms, By Country, 2012–2024

- Exports, In Value Terms, By Country, 2012–2024

- Export Prices, By Country, 2012–2024