Portable Speaker Brands: JBL and Soundcore Dominate 42% of Sales, Premium Bose Commands 2.5X Market Price

In the dynamic and rapidly expanding portable speaker market, characterized by heightened consumer demand for audio quality and mobility, understanding brand positioning is critical for strategic decision-making. This analysis leverages granular marketplace data to dissect the competitive landscape, providing actionable insights for portfolio optimization, pricing strategy, and marketing investment. The growth of e-commerce, coupled with shifting consumer preferences towards wireless and durable audio solutions, underscores the necessity for data-driven brand management. Macroeconomic factors, including inflationary pressures, further influence purchasing behavior, making price elasticity a key consideration. The analysis is geographically contextualized by data sourced from the Amazon US marketplace, with delivery parameters set to ZIP code 60007, which may reflect specific regional availability, logistical cost structures, and localized competitive intensity.

Methodology

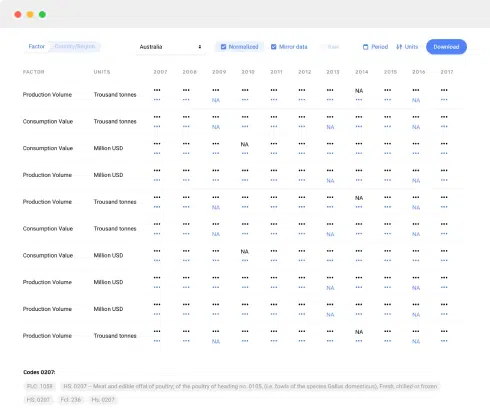

The data underpinning this analysis is sourced exclusively from IndexBox market intelligence platform, which provides real-time monitoring of the Amazon marketplace in the United States. The dataset was collected for the product category "Portable Speakers" using relevant search keywords, with the delivery location specified as ZIP code 60007. This ZIP code provides a specific lens on inventory availability, shipping dynamics, and regional pricing. All visualizations and aggregated metrics, including median values for rating, reviews, price, and sales volume, are generated from this dataset. For a deeper dive into the brand-level data, the full dataset is accessible via the IndexBox platform at: https://app.indexbox.io/brands/851822/840.

Rating vs Reviews: Mapping Brand Perception and Momentum

The scatter plot reveals four distinct brand archetypes based on the median rating (4.26) and median review count (119.6). The "Star" quadrant (High Rating/High Reviews) is occupied solely by Monster, indicating a strong market presence bolstered by positive consumer sentiment. Brands like JBL, W-KING, Soundcore, and Bose reside in the "Niche" quadrant (High Rating/Low Reviews); they have earned excellent reputations but have not yet achieved the review volume of mass-market leaders, suggesting a potential for growth through increased marketing and distribution. The "Rising" quadrant (Low Rating/High Reviews) contains Sony, Ultimate Ears, Altec Lansing, and Pyle; these brands generate significant volume and awareness, but their lower average ratings point to potential issues with product quality or customer experience that must be addressed to convert sales into loyalty. Rockville sits alone in the "Problematic" quadrant (Low Rating/Low Reviews), indicating weak market traction and perception.

Strategic recommendations vary by quadrant. "Star" brands like Monster should focus on leveraging their social proof in marketing campaigns and exploring brand extensions. "Niche" players such as JBL and Bose must invest in awareness-driving activities like influencer partnerships and targeted digital advertising to convert their high quality into higher review volume and market share. "Rising" brands, particularly Sony and Ultimate Ears, need to prioritize quality control and implement robust post-purchase engagement strategies, including proactive response to negative feedback and loyalty programs, to improve their rating. "Problematic" brands require a fundamental reassessment of their product-market fit and value proposition.

Price vs Sales Volume: Decoding Pricing Strategies and Elasticity

The analysis of average price against sales volume, with dot size representing the number of SKUs, uncovers clear strategic clusters. JBL and Bose successfully execute a "High Price/High Volume" strategy, commanding premium prices (avg. $212 and $334 respectively) while maintaining strong sales volumes, indicating powerful brand equity and inelastic demand within their segments. Conversely, Soundcore, Monster, and Ultimate Ears exemplify a "Low Price/High Volume" approach, competing on value and volume, which suggests a more elastic demand curve. Brands like Sony, W-KING, and Rockville are in the "High Price/Low Volume" trap, where their premium pricing is not justified by sufficient brand strength or product differentiation to drive volume, making them vulnerable. Pyle and Altec Lansing occupy the "Low Price/Low Volume" space, struggling to compete effectively even on price.

The wide assortment of brands like JBL (251 offers) and Pyle (234 offers) indicates a strategy of capturing multiple consumer segments but also carries a high risk of internal cannibalization. Recommendations include optimizing SKU count to focus on bestsellers for volume-driven brands and creating clearer tiering for premium brands like Bose to protect their high-margin products. Brands in the "High Price/Low Volume" quadrant must either justify their price point through enhanced innovation and marketing or reconsider their positioning to drive volume.

Price Distribution: Identifying the Market's Sweet Spots

The price distribution histogram and Kernel Density Estimate (KDE) curve show a highly right-skewed market, with the vast majority of products concentrated below the $250 mark. The primary "sweet spot" for mass-market volume lies between approximately $100 and $200, where consumer demand is most dense. A secondary, smaller peak appears in the premium segment around $350-$400, likely representing high-end brands like Bose and specialized, feature-rich models from others. The long tail of products priced above $500 shows very low density, representing a niche luxury or professional segment.

Notable anomalies in the distribution, such as isolated products at extreme price points (e.g., over $1000), could indicate limited editions, bundled offerings, or potential risks like grey market imports or pricing errors that warrant investigation. For assortment segmentation, brands should anchor their core offerings within the $100-$200 range to maximize addressable market. Premium brands can target the $300-$400 niche but must ensure exceptional product differentiation. Testing scenarios of a ±10% price change within these key ranges is crucial to understand precise elasticity and maximize revenue.

Market Share: A Concentrated Battlefield with Hidden Opportunities

JBL's commanding 38% share of total sales volume underscores its market dominance, effectively making it the category benchmark. Soundcore (9%) and Anker (8%) follow as strong volume players, leveraging their value proposition. The combined share of the top 3 brands (55%) indicates a moderately concentrated market where leadership provides significant scale advantages. The "Others" segment holds a substantial 13% share, which upon deeper analysis likely consists of smaller brands and private-label manufacturers. Breaking down this segment would reveal the next wave of competitors, such as DOSS, OontZ, or Tribit, who are often aggressive on price and quick to adopt trends.

For leaders like JBL, the strategy must be defensive: fortifying their position through innovation, brand building, and portfolio management to prevent share erosion. Challengers like Soundcore should focus on disruptive innovation and targeted marketing to steal share from the leader. For brands within the "Others" category, the opportunity lies in niche differentiation—focusing on specific use cases (e.g., ultra-rugged, shower-specific) or underserved customer segments to build a defensible position before attempting to challenge the volume giants.

Price Dispersion: Managing Assortment and Perceived Value

The boxplot analysis of the top 5 brands by offer count reveals starkly different assortment and pricing strategies. Sony exhibits the widest price range (from $38 to nearly $1000) and the highest number of high-value outliers, indicating a broad portfolio that spans from entry-level to ultra-premium, professional-grade equipment. JBL also shows a wide range but with a tighter interquartile range, suggesting a more focused core lineup despite a large number of SKUs. In contrast, brands like W-KING and Pyle operate in much narrower, lower-price bands, competing purely on value. Rockville's positioning is entirely mid-to-high-end.

Significant overlap in the interquartile ranges of JBL, W-KING, and Pyle creates a high risk of price-based competition and consumer confusion. Recommendations include rationalizing SKUs to reduce internal competition, creating clearer price-tier differentiators with corresponding feature benefits, and using limited edition or premium outliers (like Sony's high-end models) as halo products to enhance brand image rather than as volume drivers.

Actioning Intelligence: The Power of Custom Search

The static analysis provided here is merely a snapshot. The true competitive advantage comes from continuous monitoring, which is enabled by IndexBox's "Custom Search Request" panel. For instance, a marketing director can use this function to configure and automate daily parsing of specific competitor SKUs, tracking their price promotions, discount cycles, and inventory status in real-time. This data can be fed directly into a BI dashboard, triggering alerts for when a key competitor drops their price, enabling a swift and data-informed response. This automation transforms market intelligence from a periodic report into a live strategic asset.

Conclusion

The portable speaker market is a tale of two strategies: volume-driven value and premium branding, with JBL successfully straddling both. The analysis confirms that brand equity, not just price, is a primary driver of volume at higher price points. For investors, the market presents opportunities in supporting challenger brands that are cracking the code on quality and value (e.g., Soundcore) and in platforms that enable better price and promotion intelligence. Significant barriers to entry exist due to the marketing spend required to compete with established leaders and the engineering expertise needed to deliver quality audio. Ultimately, sustained success requires a commitment to product excellence, a clear and defensible pricing strategy, and the ability to leverage tools like IndexBox for ongoing, dynamic market analysis.

1. INTRODUCTION

Making Data-Driven Decisions to Grow Your Business

- REPORT DESCRIPTION

- RESEARCH METHODOLOGY AND THE AI PLATFORM

- DATA-DRIVEN DECISIONS FOR YOUR BUSINESS

- GLOSSARY AND SPECIFIC TERMS

2. EXECUTIVE SUMMARY

A Quick Overview of Market Performance

- KEY FINDINGS

- MARKET TRENDSThis Chapter is Available Only for the Professional EditionPRO

3. MARKET OVERVIEW

Understanding the Current State of The Market and its Prospects

- MARKET SIZE: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- MARKET STRUCTURE: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- TRADE BALANCE: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- PER CAPITA CONSUMPTION: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- MARKET FORECAST TO 2035

4. MOST PROMISING PRODUCTS FOR DIVERSIFICATION

Finding New Products to Diversify Your Business

- TOP PRODUCTS TO DIVERSIFY YOUR BUSINESS

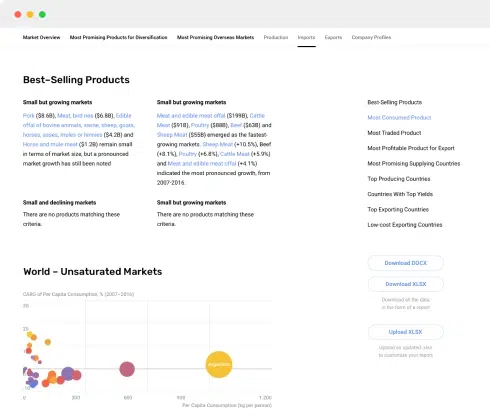

- BEST-SELLING PRODUCTS

- MOST CONSUMED PRODUCTS

- MOST TRADED PRODUCTS

- MOST PROFITABLE PRODUCTS FOR EXPORTS

5. MOST PROMISING SUPPLYING COUNTRIES

Choosing the Best Countries to Establish Your Sustainable Supply Chain

- TOP COUNTRIES TO SOURCE YOUR PRODUCT

- TOP PRODUCING COUNTRIES

- TOP EXPORTING COUNTRIES

- LOW-COST EXPORTING COUNTRIES

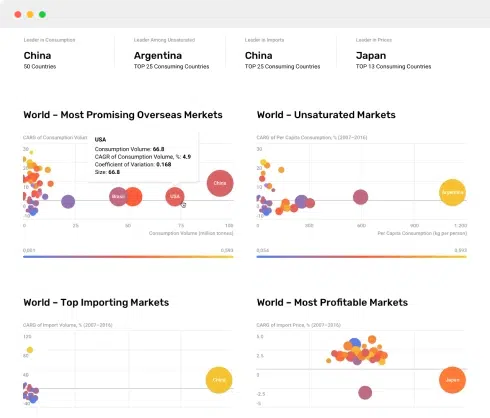

6. MOST PROMISING OVERSEAS MARKETS

Choosing the Best Countries to Boost Your Export

- TOP OVERSEAS MARKETS FOR EXPORTING YOUR PRODUCT

- TOP CONSUMING MARKETS

- UNSATURATED MARKETS

- TOP IMPORTING MARKETS

- MOST PROFITABLE MARKETS

7. PRODUCTION

The Latest Trends and Insights into The Industry

- PRODUCTION VOLUME AND VALUE: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

8. IMPORTS

The Largest Import Supplying Countries

- IMPORTS: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- IMPORTS BY COUNTRY: HISTORICAL DATA (2012–2024)

- IMPORT PRICES BY COUNTRY: HISTORICAL DATA (2012–2024)

9. EXPORTS

The Largest Destinations for Exports

- EXPORTS: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- EXPORTS BY COUNTRY: HISTORICAL DATA (2012–2024)

- EXPORT PRICES BY COUNTRY: HISTORICAL DATA (2012–2024)

10. PROFILES OF MAJOR PRODUCERS

The Largest Producers on The Market and Their Profiles

LIST OF TABLES

- Key Findings In 2024

- Market Volume, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Market Value: Historical Data (2012–2024) and Forecast (2025–2035)

- Per Capita Consumption: Historical Data (2012–2024) and Forecast (2025–2035)

- Imports, In Physical Terms, By Country, 2012–2024

- Imports, In Value Terms, By Country, 2012–2024

- Import Prices, By Country, 2012–2024

- Exports, In Physical Terms, By Country, 2012–2024

- Exports, In Value Terms, By Country, 2012–2024

- Export Prices, By Country, 2012–2024

LIST OF FIGURES

- Market Volume, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Market Value: Historical Data (2012–2024) and Forecast (2025–2035)

- Market Structure – Domestic Supply vs. Imports, in Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Market Structure – Domestic Supply vs. Imports, in Value Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Trade Balance, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Trade Balance, In Value Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Per Capita Consumption: Historical Data (2012–2024) and Forecast (2025–2035)

- Market Volume Forecast to 2035

- Market Value Forecast to 2035

- Market Size and Growth, By Product

- Average Per Capita Consumption, By Product

- Exports and Growth, By Product

- Export Prices and Growth, By Product

- Production Volume and Growth

- Exports and Growth

- Export Prices and Growth

- Market Size and Growth

- Per Capita Consumption

- Imports and Growth

- Import Prices

- Production, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Production, In Value Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Imports, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Imports, In Value Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Imports, In Physical Terms, By Country, 2024

- Imports, In Physical Terms, By Country, 2012–2024

- Imports, In Value Terms, By Country, 2012–2024

- Import Prices, By Country, 2012–2024

- Exports, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Exports, In Value Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Exports, In Physical Terms, By Country, 2024

- Exports, In Physical Terms, By Country, 2012–2024

- Exports, In Value Terms, By Country, 2012–2024

- Export Prices, By Country, 2012–2024