Portable Speaker Market Analysis: Monster Leads in Ratings and Volume

According to a report from Barchart, Exxon Mobil Corporation (XOM), with a market capitalization of $494.3 billion, is a global energy company involved in exploring, producing, and selling crude oil, natural gas, and petrochemicals. The company operates through Upstream, Energy Products, Chemical Products, and Specialty Products segments and is also developing lower-emission initiatives like carbon capture, hydrogen, and lithium.

Over the past 52 weeks, Exxon Mobil's stock performance has trailed the broader market, declining 3.3% while the S&P 500 Index ($SPX) gained 18.3%. Year-to-date, shares are up 6.9%, compared to the SPX's 17.2% gain. The company also underperformed the Energy Select Sector SPDR Fund (XLE), which fell 2.1% over the same 52-week period.

The stock experienced a 1.8% drop following its second-quarter 2025 earnings report, despite an earnings per share of $1.64 that exceeded expectations. Revenue of $81.5 billion missed estimates, attributed to weaker oil prices. Earnings from oil and gas production fell to $5.4 billion, indicating margin pressure even as the company achieved a record quarterly production of 4.6 million barrels of oil equivalent per day.

For the full 2025 fiscal year, analysts project Exxon Mobil's EPS will decrease 12.8% year-over-year to $6.79. The company has a history of surpassing earnings estimates, having beaten consensus expectations in each of the last four quarters.

Analyst sentiment remains generally positive. Among the 27 analysts covering the stock, the consensus rating is "Moderate Buy," comprised of 15 "Strong Buy" ratings, one "Moderate Buy," 10 "Holds," and one "Strong Sell." On October 9, Scotiabank raised its price target for Exxon Mobil to $128, maintaining an "Outperform" rating. The mean price target is $126.52, suggesting a nearly 10% premium to the current price, while the Street-high target of $156 implies a potential 35.6% upside.

1. INTRODUCTION

Making Data-Driven Decisions to Grow Your Business

- REPORT DESCRIPTION

- RESEARCH METHODOLOGY AND THE AI PLATFORM

- DATA-DRIVEN DECISIONS FOR YOUR BUSINESS

- GLOSSARY AND SPECIFIC TERMS

2. EXECUTIVE SUMMARY

A Quick Overview of Market Performance

- KEY FINDINGS

- MARKET TRENDSThis Chapter is Available Only for the Professional EditionPRO

3. MARKET OVERVIEW

Understanding the Current State of The Market and its Prospects

- MARKET SIZE: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- MARKET STRUCTURE: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- TRADE BALANCE: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- PER CAPITA CONSUMPTION: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- MARKET FORECAST TO 2035

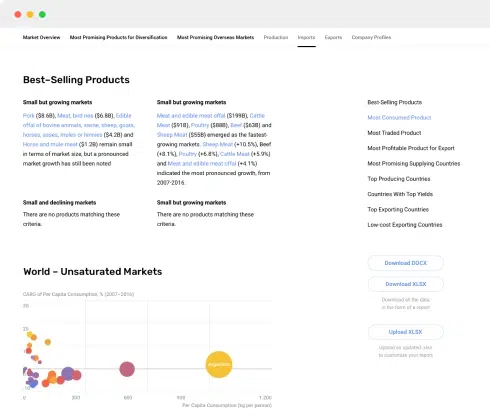

4. MOST PROMISING PRODUCTS FOR DIVERSIFICATION

Finding New Products to Diversify Your Business

- TOP PRODUCTS TO DIVERSIFY YOUR BUSINESS

- BEST-SELLING PRODUCTS

- MOST CONSUMED PRODUCTS

- MOST TRADED PRODUCTS

- MOST PROFITABLE PRODUCTS FOR EXPORTS

5. MOST PROMISING SUPPLYING COUNTRIES

Choosing the Best Countries to Establish Your Sustainable Supply Chain

- TOP COUNTRIES TO SOURCE YOUR PRODUCT

- TOP PRODUCING COUNTRIES

- TOP EXPORTING COUNTRIES

- LOW-COST EXPORTING COUNTRIES

6. MOST PROMISING OVERSEAS MARKETS

Choosing the Best Countries to Boost Your Export

- TOP OVERSEAS MARKETS FOR EXPORTING YOUR PRODUCT

- TOP CONSUMING MARKETS

- UNSATURATED MARKETS

- TOP IMPORTING MARKETS

- MOST PROFITABLE MARKETS

7. PRODUCTION

The Latest Trends and Insights into The Industry

- PRODUCTION VOLUME AND VALUE: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

8. IMPORTS

The Largest Import Supplying Countries

- IMPORTS: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- IMPORTS BY COUNTRY: HISTORICAL DATA (2012–2024)

- IMPORT PRICES BY COUNTRY: HISTORICAL DATA (2012–2024)

9. EXPORTS

The Largest Destinations for Exports

- EXPORTS: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- EXPORTS BY COUNTRY: HISTORICAL DATA (2012–2024)

- EXPORT PRICES BY COUNTRY: HISTORICAL DATA (2012–2024)

10. PROFILES OF MAJOR PRODUCERS

The Largest Producers on The Market and Their Profiles

LIST OF TABLES

- Key Findings In 2024

- Market Volume, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Market Value: Historical Data (2012–2024) and Forecast (2025–2035)

- Per Capita Consumption: Historical Data (2012–2024) and Forecast (2025–2035)

- Imports, In Physical Terms, By Country, 2012–2024

- Imports, In Value Terms, By Country, 2012–2024

- Import Prices, By Country, 2012–2024

- Exports, In Physical Terms, By Country, 2012–2024

- Exports, In Value Terms, By Country, 2012–2024

- Export Prices, By Country, 2012–2024

LIST OF FIGURES

- Market Volume, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Market Value: Historical Data (2012–2024) and Forecast (2025–2035)

- Market Structure – Domestic Supply vs. Imports, in Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Market Structure – Domestic Supply vs. Imports, in Value Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Trade Balance, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Trade Balance, In Value Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Per Capita Consumption: Historical Data (2012–2024) and Forecast (2025–2035)

- Market Volume Forecast to 2035

- Market Value Forecast to 2035

- Market Size and Growth, By Product

- Average Per Capita Consumption, By Product

- Exports and Growth, By Product

- Export Prices and Growth, By Product

- Production Volume and Growth

- Exports and Growth

- Export Prices and Growth

- Market Size and Growth

- Per Capita Consumption

- Imports and Growth

- Import Prices

- Production, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Production, In Value Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Imports, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Imports, In Value Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Imports, In Physical Terms, By Country, 2024

- Imports, In Physical Terms, By Country, 2012–2024

- Imports, In Value Terms, By Country, 2012–2024

- Import Prices, By Country, 2012–2024

- Exports, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Exports, In Value Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Exports, In Physical Terms, By Country, 2024

- Exports, In Physical Terms, By Country, 2012–2024

- Exports, In Value Terms, By Country, 2012–2024

- Export Prices, By Country, 2012–2024