Lysol and Swiffer Dominate 21% of Cleaning Products Market, While Zep Commands a 95% Premium in Niche Segments

In the dynamic and highly competitive landscape of the cleaning products market, a deep understanding of brand positioning is paramount for strategic decision-making. The accelerated growth of e-commerce, particularly on major marketplaces like Amazon, has fundamentally altered consumer purchasing behavior, placing a premium on data-driven insights. This analysis leverages granular data to dissect the performance of leading brands, evaluating their standing across critical dimensions such as consumer perception, pricing strategy, and sales volume. The objective is to provide actionable intelligence for brand managers, marketers, and investors seeking to optimize their market approach, identify growth opportunities, and mitigate competitive threats. The macroeconomic environment, characterized by inflationary pressures and shifting consumer priorities towards value and efficacy, further underscores the necessity of this rigorous examination.

The data underpinning this report is sourced from IndexBox's comprehensive monitoring tools, which aggregate and analyze listings from the Amazon marketplace in the United States. The dataset reflects the market conditions with a delivery location of ZIP code 60007, a factor that can influence product availability, shipping costs, and promotional offers, providing a precise snapshot of the competitive field. The data is collected by product categories based on specified search keywords relevant to the cleaning products segment. For a live view of the brand landscape and ongoing monitoring, the data can be explored further at: https://app.indexbox.io/brands/3402/840.

Methodology

This analysis is based on aggregated data obtained from IndexBox's proprietary monitoring tools, which track and parse product listings on the Amazon US marketplace. The dataset is filtered for the cleaning products category, with the delivery location set to ZIP code 60007 to ensure a consistent and comparable view of availability and pricing. Key metrics analyzed include average customer rating, number of reviews, average price, sales volume, and the number of individual offers per brand. The data is normalized and segmented to identify patterns and correlations that reveal strategic brand positions. All monetary values are denoted in US Dollars (USD).

Rating vs Reviews: Mapping Brand Perception and Engagement

The scatter plot of Rating versus Reviews segments brands into four distinct quadrants, each requiring a tailored strategic approach. The Star quadrant, characterized by high ratings and high review volume, includes brands like Mrs. MEYERS (4.68 rating, 140 reviews) and Weiman (4.55 rating, 162 reviews). These brands have successfully converted product quality into strong consumer advocacy. Their marketing should focus on leveraging social proof through user-generated content and ambassador programs to maintain momentum. The Rising quadrant, featuring high volume but lower relative ratings, is occupied by giants like CLOROX (4.50 rating, 193 reviews) and Mr. Clean (4.47 rating, 175 reviews). For these brands, the volume indicates strong market penetration, but the rating suggests potential issues with product consistency or customer expectation management. A critical initiative must be a robust system for addressing negative feedback and implementing quality improvements based on recurring review themes.

The Niche quadrant contains brands with excellent ratings but fewer reviews, such as Swiffer (4.64 rating, 134 reviews) and Lysol (4.59 rating, 124 reviews). These brands possess high potential but lack broad awareness. Their strategy should involve targeted digital marketing campaigns and sampling programs to stimulate initial trial and review generation. Finally, the Problematic quadrant, with lower scores on both metrics, includes Method (4.50 rating, 105 reviews) and Zep (4.47 rating, 133 reviews). These brands require a fundamental reassessment, starting with product quality enhancements followed by aggressive review solicitation strategies to rebuild credibility. Over time, monitoring movement between these quadrants is crucial; a brand like Bona sits on the cusp of becoming a Star, indicating successful initiatives that should be doubled down on.

Price vs Sales Volume: Decoding Pricing Strategy Effectiveness

The analysis of Average Price versus Sales Volume reveals clear strategic clusters and pronounced demand elasticity. The volume leaders, Lysol ($21.57, 5,502 units) and Swiffer ($21.67, 7,805 units), exemplify a successful low-price, high-volume strategy, achieving massive scale through competitive pricing and widespread distribution. This suggests a highly elastic demand within this segment; even minor price increases could significantly impact volume. Conversely, Zep operates in a premium niche with a much higher average price ($95.85) but consequently low sales volume (618 units), indicating inelastic demand from a specialized customer segment willing to pay for perceived superior quality or professional-grade products.

The number of offers, represented by dot size, provides further insight into assortment strategy. CLOROX and Amazon Basics, with a high number of offers, create a wide net for capturing search traffic but risk cannibalizing their own sales. In contrast, a focused portfolio like that of Mr. Clean may drive more concentrated sales per SKU. Recommendations include: volume leaders should explore modest, data-driven price optimizations and bundle promotions to protect margin; premium brands like Zep must justify their price through superior marketing messaging focused on efficacy and durability; and brands with many offers should rationalize their assortment to focus on high-performing SKUs and minimize internal competition.

Price Distribution: Identifying the Market's Sweet Spot

The price distribution histogram with Kernel Density Estimation (KDE) highlights a highly right-skewed market, with the vast majority of products concentrated below the $30 price point. The density peaks sharply between $10 and $20, representing the core "sweet spot" where consumer demand is most concentrated. This range is characterized by intense competition and high price sensitivity. A secondary, smaller peak appears in the $90-$110 range, aligning with the premium positioning of brands like Zep, indicating a viable albeit much smaller niche for high-end products.

Anomalies in the long tail, with prices extending beyond $300, warrant investigation. These could represent large bulk packages, specialized commercial products, or potential grey market imports and counterfeit risks due to their significant deviation from typical market prices. Assortment segmentation recommendations are clear: mass-market brands must fiercely compete within the $10-$20 range through cost leadership and promotional agility. Premium brands should anchor their positioning in the $40-$60 range to avoid direct comparison with mass products, while clearly communicating their value proposition. All brands should monitor the extreme high-end outliers to protect their brand integrity from unauthorized sellers.

Market Share: A Battle for Volume Leadership

The market share by sales volume pie chart reveals a top-heavy market where the top two brands, Lysol (11.4%) and Swiffer (11.2%), collectively control nearly a quarter of the volume. The long tail is significant, with the "Others" category representing a substantial 32.2% of the market. This indicates a fragmented landscape where numerous smaller brands collectively wield considerable influence. For leaders like Lysol and Swiffer, the strategy must be defensive, focusing on portfolio innovation, securing exclusive shelf space (both digital and physical), and leveraging economies of scale in marketing spend to maintain their dominance.

The large "Others" segment represents both a threat and an opportunity. A deeper breakdown would likely reveal emerging brands and private labels (like Amazon Basics at 7.8%) that are gaining traction. Leaders should consider acquisition strategies to absorb innovative competitors. For smaller brands within the "Others" category, the strategy is to identify underserved niches—whether based on ingredient transparency (e.g., eco-friendly), specific use cases, or unique formats—and dominate them rather than competing head-on with the giants on price. Portfolio diversification for larger players should involve creating or acquiring brands that target these specific niches to capture value across the entire market spectrum.

Price Distribution by Brand: Analyzing Assortment Width and Premium Potential

The boxplot analysis of price distribution by top brands reveals starkly different assortment and pricing strategies. Zep displays an extremely wide interquartile range and the highest median price ($36.99), confirming its premium and professional-grade positioning, though the presence of extreme high-end outliers (>$2500) suggests potential data noise or highly specialized product listings. In contrast, Lysol maintains a tight, low-priced range (median: $14.89), consistent with its mass-market, value-oriented strategy. Mrs. MEYERS and Weiman occupy the middle ground with moderately priced, focused assortments.

The significant overlap in the price ranges of Mrs. MEYERS, CLOROX, and Weiman indicates a highly competitive mid-tier segment where differentiation must be achieved through brand messaging and product features rather than price alone. Recommendations for assortment adjustment include: Zep should consider introducing a more accessible product line to capture mid-tier consumers without diluting its core premium brand. Lysol could explore a limited-edition premium sub-brand to capture margin in higher price brackets. All brands should analyze their outlier SKUs—the extremely high-priced items—to determine if they represent genuine market opportunities or are simply pricing errors that confuse consumers and dilute brand positioning.

Leveraging Custom Search Requests for Dynamic Intelligence

The static analysis provided here is merely a snapshot in time. The true competitive advantage lies in continuous monitoring. The IndexBox platform's "Custom Search Request" panel enables this by allowing users to run on-demand parsing based on specific, evolving criteria. For instance, a Marketing Director can configure an API-driven alert to monitor real-time price changes or new promotional campaigns launched by key competitors like CLOROX or Lysol. This data can be fed directly into a Business Intelligence (BI) dashboard, automating the tracking of market share shifts and promotional effectiveness. This capability transforms market intelligence from a periodic report into a live strategic asset, enabling rapid response to competitive moves and emerging trends.

Conclusion and Strategic Implications

This analysis delineates a cleaning products market bifurcated into two primary strategies: low-cost/high-volume domination, led by Lysol and Swiffer, and premium/niche specialization, exemplified by Zep and Mrs. MEYERS. The key findings indicate that consumer demand is highly elastic in the mass market but becomes inelastic in specialized segments, allowing for significant price premiums. For investors, the leaders offer stable returns based on scale, while the fragmented "Others" segment presents higher-risk opportunities for identifying the next breakout brand. Barriers to entry are high in the mass market due to scale economies but are lower in niche areas where innovation and branding can win.

The critical recommendation for all market participants is the adoption of a continuous, data-driven monitoring regimen. The marketplace is not static; brand positions shift, consumer preferences evolve, and new competitors emerge. Platforms like IndexBox provide the necessary tools to move from reactive strategizing to proactive market leadership. Success will belong to those brands that can not only understand their current quadrant but also effectively navigate to the next one.

1. INTRODUCTION

Making Data-Driven Decisions to Grow Your Business

- REPORT DESCRIPTION

- RESEARCH METHODOLOGY AND THE AI PLATFORM

- DATA-DRIVEN DECISIONS FOR YOUR BUSINESS

- GLOSSARY AND SPECIFIC TERMS

2. EXECUTIVE SUMMARY

A Quick Overview of Market Performance

- KEY FINDINGS

- MARKET TRENDSThis Chapter is Available Only for the Professional EditionPRO

3. MARKET OVERVIEW

Understanding the Current State of The Market and its Prospects

- MARKET SIZE: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- MARKET STRUCTURE: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- TRADE BALANCE: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- PER CAPITA CONSUMPTION: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- MARKET FORECAST TO 2035

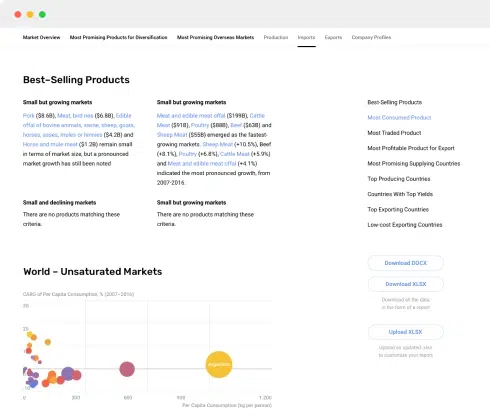

4. MOST PROMISING PRODUCTS FOR DIVERSIFICATION

Finding New Products to Diversify Your Business

- TOP PRODUCTS TO DIVERSIFY YOUR BUSINESS

- BEST-SELLING PRODUCTS

- MOST CONSUMED PRODUCTS

- MOST TRADED PRODUCTS

- MOST PROFITABLE PRODUCTS FOR EXPORTS

5. MOST PROMISING SUPPLYING COUNTRIES

Choosing the Best Countries to Establish Your Sustainable Supply Chain

- TOP COUNTRIES TO SOURCE YOUR PRODUCT

- TOP PRODUCING COUNTRIES

- TOP EXPORTING COUNTRIES

- LOW-COST EXPORTING COUNTRIES

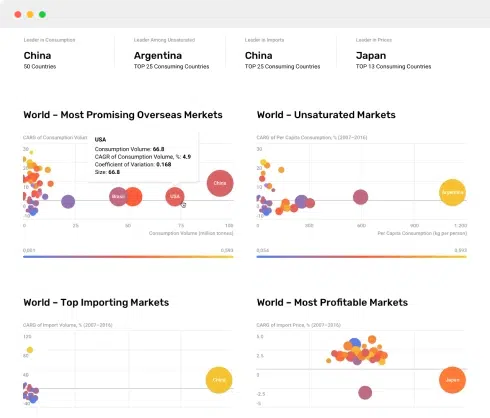

6. MOST PROMISING OVERSEAS MARKETS

Choosing the Best Countries to Boost Your Export

- TOP OVERSEAS MARKETS FOR EXPORTING YOUR PRODUCT

- TOP CONSUMING MARKETS

- UNSATURATED MARKETS

- TOP IMPORTING MARKETS

- MOST PROFITABLE MARKETS

7. PRODUCTION

The Latest Trends and Insights into The Industry

- PRODUCTION VOLUME AND VALUE: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

8. IMPORTS

The Largest Import Supplying Countries

- IMPORTS: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- IMPORTS BY COUNTRY: HISTORICAL DATA (2012–2024)

- IMPORT PRICES BY COUNTRY: HISTORICAL DATA (2012–2024)

9. EXPORTS

The Largest Destinations for Exports

- EXPORTS: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- EXPORTS BY COUNTRY: HISTORICAL DATA (2012–2024)

- EXPORT PRICES BY COUNTRY: HISTORICAL DATA (2012–2024)

10. PROFILES OF MAJOR PRODUCERS

The Largest Producers on The Market and Their Profiles

LIST OF TABLES

- Key Findings In 2024

- Market Volume, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Market Value: Historical Data (2012–2024) and Forecast (2025–2035)

- Per Capita Consumption: Historical Data (2012–2024) and Forecast (2025–2035)

- Imports, In Physical Terms, By Country, 2012–2024

- Imports, In Value Terms, By Country, 2012–2024

- Import Prices, By Country, 2012–2024

- Exports, In Physical Terms, By Country, 2012–2024

- Exports, In Value Terms, By Country, 2012–2024

- Export Prices, By Country, 2012–2024

LIST OF FIGURES

- Market Volume, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Market Value: Historical Data (2012–2024) and Forecast (2025–2035)

- Market Structure – Domestic Supply vs. Imports, in Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Market Structure – Domestic Supply vs. Imports, in Value Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Trade Balance, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Trade Balance, In Value Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Per Capita Consumption: Historical Data (2012–2024) and Forecast (2025–2035)

- Market Volume Forecast to 2035

- Market Value Forecast to 2035

- Market Size and Growth, By Product

- Average Per Capita Consumption, By Product

- Exports and Growth, By Product

- Export Prices and Growth, By Product

- Production Volume and Growth

- Exports and Growth

- Export Prices and Growth

- Market Size and Growth

- Per Capita Consumption

- Imports and Growth

- Import Prices

- Production, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Production, In Value Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Imports, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Imports, In Value Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Imports, In Physical Terms, By Country, 2024

- Imports, In Physical Terms, By Country, 2012–2024

- Imports, In Value Terms, By Country, 2012–2024

- Import Prices, By Country, 2012–2024

- Exports, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Exports, In Value Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Exports, In Physical Terms, By Country, 2024

- Exports, In Physical Terms, By Country, 2012–2024

- Exports, In Value Terms, By Country, 2012–2024

- Export Prices, By Country, 2012–2024