Royal Canin and Hills Science Diet Dominate Premium Segment with 49% Price Premium, While Purina ONE Leads Volume with 3861 Units per Seller

The pet food market, a cornerstone of the rapidly expanding pet care industry, is characterized by intense competition and distinct consumer segments driven by factors such as ingredient quality, breed-specific formulations, and price sensitivity. This analysis leverages granular marketplace data to deconstruct the competitive landscape for cat and dog food brands, providing strategic insights into brand positioning, pricing elasticity, and market share dynamics. Understanding these levers is critical for manufacturers, retailers, and investors to optimize product portfolios, marketing strategies, and investment allocations in a market increasingly shaped by e-commerce and direct-to-consumer trends.

Methodology

This report is based on data aggregated by IndexBox AI-powered market intelligence platform. The dataset comprises real-time monitoring data scraped from the Amazon marketplace in the United States, with all listings and sales metrics filtered for delivery to ZIP code 60007. The product category was defined by the search keyword "Cat and Dog Food," ensuring a comprehensive view of the relevant SKUs. The data reflects a snapshot of brand performance, including average rating, review count, price, sales volume, and number of offers. For a live view of brand rankings and dynamics, the data is available at: IndexBox Brand Analysis for Cat and Dog Food.

Rating vs Reviews: Mapping Brand Perception and Engagement

The scatter plot of Rating versus Reviews segments brands into four critical quadrants, revealing their market perception and engagement health. The Star quadrant, characterized by high ratings and high reviews, includes Royal Canin and Blue Buffalo; these brands have successfully converted product quality into broad consumer trust and advocacy, creating a powerful barrier to entry for competitors. The Niche quadrant, featuring high ratings but lower reviews, contains Hills Science Diet, Pedigree, and IAMS; these brands enjoy strong customer satisfaction but have not yet achieved the same level of market penetration or review velocity, indicating a potential awareness gap. The Rising quadrant, with high review counts but lower average ratings, includes Wellness, Purina Pro Plan, and Merrick; this suggests high sales volume and trial but also points to consistent product or expectation mismatches that are generating negative feedback. The Problematic quadrant, with low ratings and low reviews, is occupied by Purina ONE and Nutrish, indicating a lack of both market presence and strong consumer advocacy.

Strategic recommendations vary significantly by quadrant. Star brands should focus on leveraging their social proof in marketing campaigns and exploring premium line extensions to maximize customer lifetime value. Niche brands must invest in targeted digital marketing and sampling programs to drive awareness and conversion, thereby increasing their review volume. Rising brands require immediate investment in quality control and customer service, actively soliciting and addressing negative feedback to improve their rating before it damages long-term brand equity. Problematic brands need a fundamental reassessment of their product-market fit, potentially involving reformulation and aggressive promotional strategies to stimulate trial and gather more data.

Price vs Sales Volume: Decoding Pricing Strategies and Elasticity

The analysis of Average Price versus Sales Volume, with dot size representing the number of distinct offers, uncovers clear strategic clusters. The High Price / High Volume quadrant is the most desirable, occupied by Purina ONE and Hills Science Diet; these brands command premium prices while achieving massive sales volumes, indicating strong brand equity and inelastic demand for their perceived quality. The Low Price / High Volume quadrant includes Nutrish, IAMS, and Pedigree, pursuing a value-based volume strategy that relies on high turnover and competitive pricing. The High Price / Low Volume quadrant features Royal Canin, Purina Pro Plan, and Merrick; this is a classic premium niche strategy, focusing on margin over volume, often targeting specific health conditions or breeds. Finally, the Low Price / Low Volume quadrant contains Blue Buffalo and Wellness, a challenging position that suggests a mismatch between pricing, product offering, and market appeal.

The elasticity of demand appears to vary dramatically. The success of Purina ONE demonstrates that the market supports premium pricing when coupled with high volume, suggesting marketing efforts are effectively communicating value. Conversely, Blue Buffalo's position indicates its current price point may be too high for its perceived value, suppressing volume. The large number of offers for Blue Buffalo and Royal Canin also highlights a risk of assortment cannibalization, where too many SKUs compete against each other, confusing consumers and diluting sales per SKU. Recommendations include optimizing the number of active offers to focus on bestsellers for volume brands and maintaining a curated, high-margin assortment for premium players.

Price Distribution: Identifying the Market's Sweet Spot

The price distribution histogram with Kernel Density Estimate (KDE) reveals a highly concentrated and multi-modal market. The data shows a primary concentration of products in the $20-$35 range, which represents the core market "sweet spot" for mass-market brands. A significant secondary peak exists in the $40-$50 range, indicative of the premium segment occupied by brands like Royal Canin and Hills Science Diet. The long tail of prices extending beyond $70 shows a luxury or specialized medical niche with very low volume but potentially very high margins.

Anomalies in the distribution, such as products priced significantly below the typical range for their brand, could indicate the presence of grey imports, counterfeit goods, or expired products, requiring vigilant monitoring. Assortment segmentation recommendations are clear: brands should anchor their core offerings in the $20-$35 range to compete for volume, while developing clearly differentiated premium products in the $40-$50 range to capture margin. Scenario testing of a ±5% price change within these key ranges is advised to optimize for maximum revenue without triggering significant volume loss.

Market Share: A Battle for Volume Leadership

The market share by sales volume pie chart illustrates a fragmented but top-heavy landscape. Purina ONE leads with a significant share, driven by its successful high-volume, high-price strategy. Blue Buffalo follows closely, but as previously identified, its volume is achieved with a lower price point and a high number of offers, suggesting less efficiency. The long tail of competitors, including Hills Science Diet, Royal Canin, and Nutrish, holds substantial combined share, indicating that niche strategies are viable.

For leaders like Purina ONE, the strategy must be defensive: strengthening brand loyalty through innovation and customer engagement to protect its top position. For challengers like Blue Buffalo, portfolio rationalization is key to improving margin while maintaining share. For smaller brands and those in the "Others" segment, the opportunity lies in extreme differentiation—focusing on unique ingredients, specific life stages, or health conditions to carve out a defensible niche without directly challenging the volume giants. A deeper breakdown of the "Others" basket is essential to identify emerging brands that could disrupt the established order.

Price Distribution by Brand: Analyzing Assortment and Positioning

The boxplot analysis of price distribution by top brands provides a granular view of their assortment strategy and market coverage. Royal Canin exhibits the widest interquartile range and the highest median price, firmly cementing its premium positioning while also offering products across a broad spectrum. In contrast, Purina Pro Plan shows a remarkably tight interquartile range, indicating a highly focused and consistent premium pricing strategy with little variance. Blue Buffalo and Wellness display significant price dispersion, with Wellness having a very long lower tail, suggesting attempts to compete in value segments may be diluting their core brand positioning.

The presence of high-value outliers, particularly for Royal Canin, indicates specialized prescription or limited-edition lines that serve as halo products and margin drivers. The significant overlap in the price ranges of Blue Buffalo, Wellness, and Purina Pro Plan creates a highly competitive zone ripe for price wars. Recommendations include optimizing price ranges to minimize destructive overlap: Blue Buffalo could benefit from tightening its range to focus on its core $25-$40 price point, while Wellness should consider segregating its value offerings into a sub-brand to protect its premium equity.

Custom Search Request: On-Demand Competitive Intelligence

The static analysis provided is powerful, but market dynamics require constant monitoring. The IndexBox platform's "Custom Search Request" panel enables this through on-demand, API-driven parsing of marketplace data. A marketing director can automate daily reports on competitor promotions for specific SKUs, tracking discounting patterns and market share shifts in near real-time. This functionality can be integrated directly into BI dashboards, allowing for automated alerts when a key competitor's price drops or when a new product launch gains significant review velocity, transforming market intelligence from a periodic exercise into a continuous competitive advantage.

Conclusion

This analysis reveals a pet food market segmented by starkly different strategies: volume-driven value players, margin-focused premium specialists, and brands struggling to find a clear positioning. Key findings indicate that Purina ONE has achieved an enviable balance of price and volume, while Royal Canin dominates the high-margin premium niche. For investors, the clear brand equity and pricing power of the premium segment present attractive opportunities, though high marketing spend is a barrier to entry for new players. The consistent recommendation across all analyses is the critical need for continuous, automated market monitoring through a platform like IndexBox to quickly adapt to competitor moves, optimize pricing, and protect hard-earned market positions.

1. INTRODUCTION

Making Data-Driven Decisions to Grow Your Business

- REPORT DESCRIPTION

- RESEARCH METHODOLOGY AND THE AI PLATFORM

- DATA-DRIVEN DECISIONS FOR YOUR BUSINESS

- GLOSSARY AND SPECIFIC TERMS

2. EXECUTIVE SUMMARY

A Quick Overview of Market Performance

- KEY FINDINGS

- MARKET TRENDSThis Chapter is Available Only for the Professional EditionPRO

3. MARKET OVERVIEW

Understanding the Current State of The Market and its Prospects

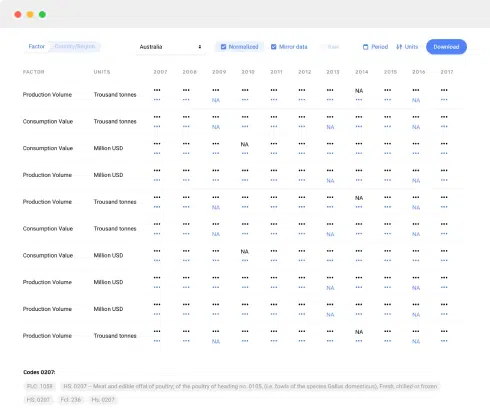

- MARKET SIZE: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- MARKET STRUCTURE: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- TRADE BALANCE: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- PER CAPITA CONSUMPTION: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- MARKET FORECAST TO 2035

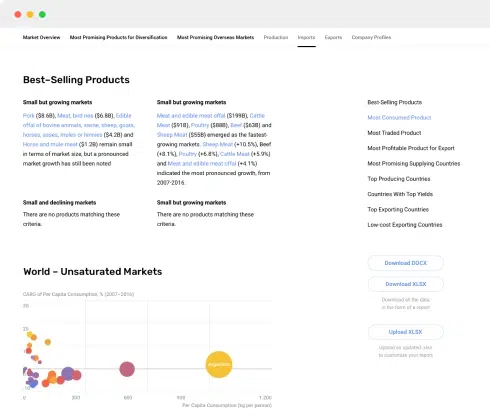

4. MOST PROMISING PRODUCTS FOR DIVERSIFICATION

Finding New Products to Diversify Your Business

- TOP PRODUCTS TO DIVERSIFY YOUR BUSINESS

- BEST-SELLING PRODUCTS

- MOST CONSUMED PRODUCTS

- MOST TRADED PRODUCTS

- MOST PROFITABLE PRODUCTS FOR EXPORTS

5. MOST PROMISING SUPPLYING COUNTRIES

Choosing the Best Countries to Establish Your Sustainable Supply Chain

- TOP COUNTRIES TO SOURCE YOUR PRODUCT

- TOP PRODUCING COUNTRIES

- TOP EXPORTING COUNTRIES

- LOW-COST EXPORTING COUNTRIES

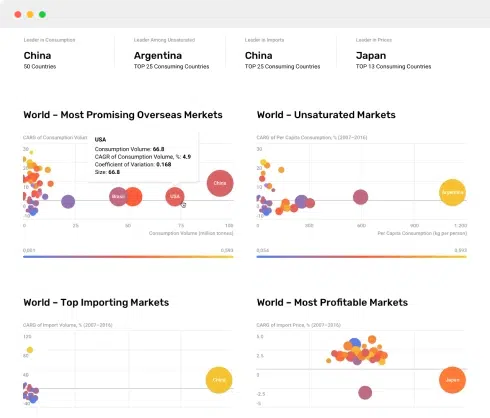

6. MOST PROMISING OVERSEAS MARKETS

Choosing the Best Countries to Boost Your Export

- TOP OVERSEAS MARKETS FOR EXPORTING YOUR PRODUCT

- TOP CONSUMING MARKETS

- UNSATURATED MARKETS

- TOP IMPORTING MARKETS

- MOST PROFITABLE MARKETS

7. PRODUCTION

The Latest Trends and Insights into The Industry

- PRODUCTION VOLUME AND VALUE: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

8. IMPORTS

The Largest Import Supplying Countries

- IMPORTS: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- IMPORTS BY COUNTRY: HISTORICAL DATA (2012–2024)

- IMPORT PRICES BY COUNTRY: HISTORICAL DATA (2012–2024)

9. EXPORTS

The Largest Destinations for Exports

- EXPORTS: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- EXPORTS BY COUNTRY: HISTORICAL DATA (2012–2024)

- EXPORT PRICES BY COUNTRY: HISTORICAL DATA (2012–2024)

10. PROFILES OF MAJOR PRODUCERS

The Largest Producers on The Market and Their Profiles

LIST OF TABLES

- Key Findings In 2024

- Market Volume, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Market Value: Historical Data (2012–2024) and Forecast (2025–2035)

- Per Capita Consumption: Historical Data (2012–2024) and Forecast (2025–2035)

- Imports, In Physical Terms, By Country, 2012–2024

- Imports, In Value Terms, By Country, 2012–2024

- Import Prices, By Country, 2012–2024

- Exports, In Physical Terms, By Country, 2012–2024

- Exports, In Value Terms, By Country, 2012–2024

- Export Prices, By Country, 2012–2024

LIST OF FIGURES

- Market Volume, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Market Value: Historical Data (2012–2024) and Forecast (2025–2035)

- Market Structure – Domestic Supply vs. Imports, in Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Market Structure – Domestic Supply vs. Imports, in Value Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Trade Balance, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Trade Balance, In Value Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Per Capita Consumption: Historical Data (2012–2024) and Forecast (2025–2035)

- Market Volume Forecast to 2035

- Market Value Forecast to 2035

- Market Size and Growth, By Product

- Average Per Capita Consumption, By Product

- Exports and Growth, By Product

- Export Prices and Growth, By Product

- Production Volume and Growth

- Exports and Growth

- Export Prices and Growth

- Market Size and Growth

- Per Capita Consumption

- Imports and Growth

- Import Prices

- Production, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Production, In Value Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Imports, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Imports, In Value Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Imports, In Physical Terms, By Country, 2024

- Imports, In Physical Terms, By Country, 2012–2024

- Imports, In Value Terms, By Country, 2012–2024

- Import Prices, By Country, 2012–2024

- Exports, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Exports, In Value Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Exports, In Physical Terms, By Country, 2024

- Exports, In Physical Terms, By Country, 2012–2024

- Exports, In Value Terms, By Country, 2012–2024

- Export Prices, By Country, 2012–2024