Game Controller Market Analysis: 8Bitdo and Microsoft Lead with High Ratings and Trust

Key Findings

- Nintendo and 8Bitdo demonstrate market leadership with high ratings and significant sales volume, indicating strong brand equity and product-market fit.

- A clear market segmentation exists between low-cost, high-volume brands (e.g., PowerA, GameSir) and premium, lower-volume players (e.g., Microsoft, Razer).

- The market exhibits a multi-modal price distribution with key clusters below $60 and a long tail of premium offerings above $115.

- Significant price dispersion within brand portfolios suggests sophisticated tiering strategies but also potential for internal cannibalization.

- The "Others" category holds a substantial 11.4% volume share, representing a competitive threat from emerging or niche brands.

Methodology

The findings in this report are derived from an analysis of publicly available e-commerce data on the Amazon marketplace in the United States, with ZIP code 60007 as the delivery location. The data is collected by product categories using the search keyword "Game Controllers". For a dynamic and detailed view of brand performance metrics, refer to the Brands section of the IndexBox platform.

Rating vs Reviews

Star Brands Microsoft and 8Bitdo combine high ratings with high review counts, signaling market trust and satisfaction. These brands should focus on maintaining quality and leveraging their strong reputation for premium product launches and loyalty programs to maximize customer lifetime value.

Rising Brands HORI, Hyperkin, and Razer have high visibility (reviews) but sub-par ratings, indicating potential quality or expectation mismatches. Immediate action should include a deep analysis of negative feedback for product iteration and implementing aggressive post-purchase engagement campaigns to convert dissatisfied customers.

Niche Brands PowerA, GameSir, and Nintendo enjoy high ratings but have not yet achieved mass-market review volumes. Their strategy should focus on stimulating word-of-mouth through referral programs and targeted digital marketing to amplify their positive sentiment and drive user acquisition.

Problematic Brands Sony and PDP suffer from lower ratings and limited market buzz. A fundamental product reassessment is critical, coupled with tactical promotions to clear existing stock and rebuild brand perception from the ground up with a focus on core quality improvements.

Price vs Sales Volume

Value Volume Leaders Brands like 8Bitdo and PowerA operate in the low-price, high-volume quadrant, suggesting high price elasticity of demand. Their large number of offers (SKUs) is a key success factor, and they should continue to optimize their assortment breadth to capture volume and defend against entry-level competitors.

Premium Niche Players Microsoft, PDP, and HORI occupy the high-price, low-volume space, catering to a less price-sensitive segment. Their focus must remain on superior quality, exclusive features, and high-margin economics, avoiding volume-based price wars that would erode their brand positioning.

Market Anomalies Nintendo defies typical elasticity, commanding high volume at a premium price, a sign of exceptional brand power. Razer achieves high prices with moderate volume, leveraging its gaming ecosystem. These positions are enviable but vulnerable and require constant innovation to justify their premium.

Price Distribution

Market Sweet Spots The analysis reveals a primary mass-market cluster concentrated in the $45-$75 range, which is highly competitive. A secondary, less dense premium cluster exists above $115, catering to enthusiasts. Brands should align their core offerings within the primary cluster while using premium products for brand building and margin capture.

Strategic Segmentation The multi-modal distribution validates distinct customer segments: budget-conscious, mainstream, and premium. Assortment strategies must be tailored for each, with clear value propositions to avoid cannibalization. Testing price changes within ±10% of range boundaries can help optimize positioning without triggering segment migration.

Anomaly Vigilance The long tail of listings extending beyond $200 requires scrutiny for potential grey market imports or counterfeit products that could damage brand integrity. Monitoring these outliers is essential for protecting brand value and ensuring marketplace health.

Market Share

Leadership Defense Nintendo's volume leadership is clear, but it faces pressure from value-focused brands like GameSir. To defend its position, Nintendo should leverage its iconic IP and explore sub-brands or exclusive features that cannot be easily replicated by lower-cost competitors.

Portfolio Diversification The significant 11.4% share held by "Others" represents both a threat and an opportunity. Leaders should analyze this segment for acquisition targets or emerging trends. For smaller brands in the "Others" category, the strategy should be hyper-specialization in untapped niches or unique controller types.

Boxplot

Assortment Complexity Top brands show significant internal price dispersion, indicating multi-tier product portfolios. This is a effective strategy for market coverage but risks confusing consumers and internal cannibalization. Clear, consumer-centric tiering (e.g., Essential, Enhanced, Elite) is necessary to justify the price ranges.

Optimization Opportunities The overlapping interquartile ranges of brands like GameSir and PowerA indicate intense competition in the $25-$50 bracket. To avoid pure price competition, brands must differentiate through ergonomics, features, or design. The high-value outliers represent opportunities for limited editions or premium bundles to enhance brand perception.

Custom Search Request

The IndexBox platform's "Custom Search Request" panel enables on-demand data parsing for real-time competitive intelligence. A marketing director can automate daily monitoring of competitor promotions and pricing changes for specific brands like Razer or Nintendo via API, feeding this data directly into a BI dashboard for instantaneous strategic response, moving from reactive to proactive market engagement.

Conclusion

The game controller market is bifurcated into a high-volume value segment and a high-margin premium segment, with few brands successfully bridging the gap. Nintendo demonstrates the power of strong IP, while brands like 8Bitdo show how quality can drive volume at mid-tier prices. For investors, the value segment offers volume-based returns, while the premium niche promises higher margins but requires continuous innovation. New entrants face high barriers to entry due to established brand loyalty and the need for significant assortment breadth to compete. The analysis for ZIP code 60007 (a Chicago suburb) confirms typical national availability and logistics patterns, with no significant regional constraints affecting the broader conclusions. Regular monitoring through IndexBox is recommended to track brand movement across quadrants and respond dynamically to market shifts.

1. INTRODUCTION

Making Data-Driven Decisions to Grow Your Business

- REPORT DESCRIPTION

- RESEARCH METHODOLOGY AND THE AI PLATFORM

- DATA-DRIVEN DECISIONS FOR YOUR BUSINESS

- GLOSSARY AND SPECIFIC TERMS

2. EXECUTIVE SUMMARY

A Quick Overview of Market Performance

- KEY FINDINGS

- MARKET TRENDSThis Chapter is Available Only for the Professional EditionPRO

3. MARKET OVERVIEW

Understanding the Current State of The Market and its Prospects

- MARKET SIZE: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- MARKET STRUCTURE: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- TRADE BALANCE: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- PER CAPITA CONSUMPTION: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- MARKET FORECAST TO 2035

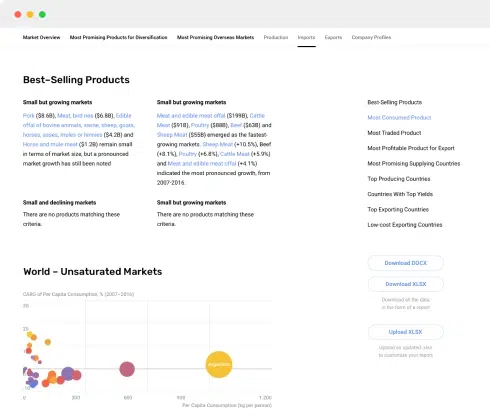

4. MOST PROMISING PRODUCTS FOR DIVERSIFICATION

Finding New Products to Diversify Your Business

- TOP PRODUCTS TO DIVERSIFY YOUR BUSINESS

- BEST-SELLING PRODUCTS

- MOST CONSUMED PRODUCTS

- MOST TRADED PRODUCTS

- MOST PROFITABLE PRODUCTS FOR EXPORTS

5. MOST PROMISING SUPPLYING COUNTRIES

Choosing the Best Countries to Establish Your Sustainable Supply Chain

- TOP COUNTRIES TO SOURCE YOUR PRODUCT

- TOP PRODUCING COUNTRIES

- TOP EXPORTING COUNTRIES

- LOW-COST EXPORTING COUNTRIES

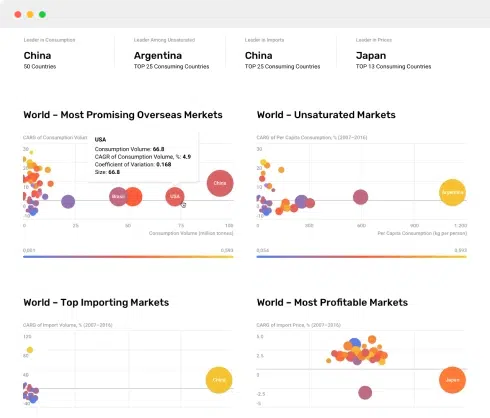

6. MOST PROMISING OVERSEAS MARKETS

Choosing the Best Countries to Boost Your Export

- TOP OVERSEAS MARKETS FOR EXPORTING YOUR PRODUCT

- TOP CONSUMING MARKETS

- UNSATURATED MARKETS

- TOP IMPORTING MARKETS

- MOST PROFITABLE MARKETS

7. PRODUCTION

The Latest Trends and Insights into The Industry

- PRODUCTION VOLUME AND VALUE: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

8. IMPORTS

The Largest Import Supplying Countries

- IMPORTS: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- IMPORTS BY COUNTRY: HISTORICAL DATA (2012–2024)

- IMPORT PRICES BY COUNTRY: HISTORICAL DATA (2012–2024)

9. EXPORTS

The Largest Destinations for Exports

- EXPORTS: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- EXPORTS BY COUNTRY: HISTORICAL DATA (2012–2024)

- EXPORT PRICES BY COUNTRY: HISTORICAL DATA (2012–2024)

10. PROFILES OF MAJOR PRODUCERS

The Largest Producers on The Market and Their Profiles

LIST OF TABLES

- Key Findings In 2024

- Market Volume, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Market Value: Historical Data (2012–2024) and Forecast (2025–2035)

- Per Capita Consumption: Historical Data (2012–2024) and Forecast (2025–2035)

- Imports, In Physical Terms, By Country, 2012–2024

- Imports, In Value Terms, By Country, 2012–2024

- Import Prices, By Country, 2012–2024

- Exports, In Physical Terms, By Country, 2012–2024

- Exports, In Value Terms, By Country, 2012–2024

- Export Prices, By Country, 2012–2024

LIST OF FIGURES

- Market Volume, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Market Value: Historical Data (2012–2024) and Forecast (2025–2035)

- Market Structure – Domestic Supply vs. Imports, in Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Market Structure – Domestic Supply vs. Imports, in Value Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Trade Balance, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Trade Balance, In Value Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Per Capita Consumption: Historical Data (2012–2024) and Forecast (2025–2035)

- Market Volume Forecast to 2035

- Market Value Forecast to 2035

- Market Size and Growth, By Product

- Average Per Capita Consumption, By Product

- Exports and Growth, By Product

- Export Prices and Growth, By Product

- Production Volume and Growth

- Exports and Growth

- Export Prices and Growth

- Market Size and Growth

- Per Capita Consumption

- Imports and Growth

- Import Prices

- Production, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Production, In Value Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Imports, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Imports, In Value Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Imports, In Physical Terms, By Country, 2024

- Imports, In Physical Terms, By Country, 2012–2024

- Imports, In Value Terms, By Country, 2012–2024

- Import Prices, By Country, 2012–2024

- Exports, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Exports, In Value Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Exports, In Physical Terms, By Country, 2024

- Exports, In Physical Terms, By Country, 2012–2024

- Exports, In Value Terms, By Country, 2012–2024

- Export Prices, By Country, 2012–2024