Dell Emerges as Sole Star in Monitor Market, Balancing High Ratings and Volume

Key Findings

Dell emerges as the sole "Star" brand, uniquely combining high customer ratings with substantial review volume, indicating strong market trust and penetration.

The market exhibits a clear segmentation into distinct price-performance quadrants, with Samsung, ASUS, and AOC dominating the high-price, high-volume premium segment.

Price distribution is heavily right-skewed, with a concentration of offers below $300, suggesting a highly competitive mass market with a long tail of premium, niche products.

Market share by sales volume is highly concentrated, with the top four brands (Sceptre, Samsung, Dell, ASUS) commanding over 80% of the market, indicating significant barriers to entry for new players.

Significant price dispersion exists within leading brands' portfolios, particularly for ASUS and Samsung, highlighting sophisticated multi-tier assortment strategies targeting different consumer segments.

Methodology

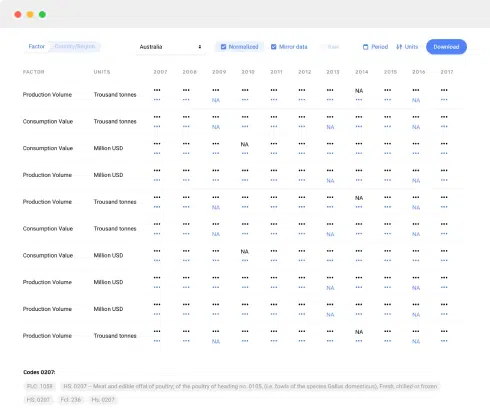

The findings in this report are derived from an analysis of publicly available e-commerce data on the Amazon marketplace in the United States, with ZIP code 60007 as the delivery location. The data is collected by product categories using the search keyword "Monitors". For a deeper dive into brand-level analytics, access the dedicated platform: IndexBox Brands Dashboard.

Rating vs Reviews

Star Brands (High Rating/High Reviews): Dell is the singular occupant of this quadrant, representing an ideal market position. This brand should focus on defending its leadership through continuous product innovation and leveraging its positive reputation to justify potential price premiums.

Rising Brands (Low Rating/High Reviews): Samsung, ASUS, Radeon, and Eyoyo have strong market presence but suffer from marginally lower ratings. Immediate action should focus on analyzing negative feedback to address quality control issues and implementing proactive customer service outreach to improve sentiment.

Niche Brands (High Rating/Low Reviews): Lenovo, AOC, HP, and Sceptre enjoy high customer satisfaction but lack market visibility. Marketing efforts should prioritize amplifying positive reviews through targeted digital campaigns and influencer partnerships to build awareness and convert high satisfaction into higher sales volume.

Problematic Brands (Low Rating/Low Reviews): SideTrak is in a precarious position with limited market traction and poor perception. A fundamental reassessment of product-market fit is recommended, potentially involving a product relaunch supported by aggressive promotional pricing to generate initial reviews and market feedback.

Price vs Sales Volume

Premium Volume Leaders: Samsung, ASUS, and AOC successfully operate in the high-price, high-volume quadrant, demonstrating inelastic demand for branded, feature-rich monitors. Their strategy should focus on maintaining perceived value through innovation and brand storytelling to justify their price points and avoid direct price competition.

Value Volume Leaders: Dell and Lenovo dominate the low-price, high-volume space, suggesting a high-volume, competitive pricing strategy. They should optimize supply chains for margin protection and explore bundle offers to increase average order value without sacrificing volume.

Niche & Problematic Segments: Brands like Alienware (high-price, low-volume) occupy a premium niche, which should be nurtured with highly targeted marketing. Low-price, low-volume brands (e.g., Radeon, CRUA) face intense competition and must differentiate through unique features or aggressive channel strategies to gain visibility.

Price Distribution

Mass Market Concentration: The distribution is intensely right-skewed, with the vast majority of products clustered below the $300 mark. This indicates a fiercely competitive mass market where economies of scale and operational efficiency are critical for profitability.

Premium Long Tail: A long tail of products extends beyond $500, representing niche segments (e.g., gaming, professional design). Brands should identify sub-$500 "sweet spots" within this range to capture margin without volume collapse, avoiding the barren price points between $600 and $900.

Assortment & Pricing Strategy: Retailers should segment their assortment clearly into value (<$200), mainstream ($200-$400), and premium (>$400) tiers. Pricing tests should be conducted in increments of 5-10% within these bands to gauge elasticity without triggering cross-tier cannibalization.

Market Share

Market Leadership: Sceptre's volume leadership, despite a weaker rating position, suggests a winning value-based proposition and distribution strategy. However, this position is vulnerable to rating erosion; the focus must be on improving product quality to convert volume into lasting brand equity.

Portfolio Diversification: Leaders like Samsung and Dell have balanced portfolios across price segments. Other brands should emulate this by developing fighter brands or SKUs to compete in high-volume tiers while protecting premium brand equity in higher-margin segments.

The "Others" Segment: The consolidated "Others" category represents a significant competitive threat. Market leaders should continuously monitor this segment to identify emerging trends and potential acquisition targets before they gain critical mass and disrupt the established order.

Boxplot Analysis

Assortment Width Strategy: ASUS and Samsung exhibit the widest price ranges, from budget to premium, indicating a comprehensive portfolio strategy targeting multiple consumer segments. This approach maximizes addressable market but requires careful brand architecture to avoid self-cannibalization.

Focused Value Proposition: Brands like Radeon show a tighter, more concentrated price range, suggesting a focused value proposition. This simplifies marketing messaging but may limit growth potential by capping the brand at a specific price point.

Optimizing Price Ranges: Significant overlap in the mid-range ($150-$350) among all brands indicates intense competition. To avoid pure price wars, brands should differentiate through features, design, or warranty services. The presence of high-value outliers (>$1000) for ASUS and Samsung validates the existence of a lucrative ultra-premium niche.

Custom Search Request

The IndexBox platform's "Custom Search Request" panel enables on-demand, targeted data parsing for scenario-based analysis. A marketing director can automate daily tracking of specific competitor SKU promotions and price changes via API, feeding this real-time data into a BI dashboard for agile decision-making and tactical response.

Conclusion

The monitor market is a tale of two strategies: volume-driven value and feature-led premium. Success requires a clear positioning within this framework, supported by operational excellence and data-driven agility. The concentration of market share and the clear segmentation present high barriers to entry for new players, who must identify an uncontested niche or leverage significant capital to compete on volume. For investors, the opportunities lie in brands with a dual ability to command premium prices and scale volume, like Samsung and Dell. Continuous monitoring through IndexBox is essential to track brand momentum, pricing shifts, and the emergence of disruptive competitors from the long tail.

1. INTRODUCTION

Making Data-Driven Decisions to Grow Your Business

- REPORT DESCRIPTION

- RESEARCH METHODOLOGY AND THE AI PLATFORM

- DATA-DRIVEN DECISIONS FOR YOUR BUSINESS

- GLOSSARY AND SPECIFIC TERMS

2. EXECUTIVE SUMMARY

A Quick Overview of Market Performance

- KEY FINDINGS

- MARKET TRENDSThis Chapter is Available Only for the Professional EditionPRO

3. MARKET OVERVIEW

Understanding the Current State of The Market and its Prospects

- MARKET SIZE: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- MARKET STRUCTURE: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- TRADE BALANCE: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- PER CAPITA CONSUMPTION: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- MARKET FORECAST TO 2035

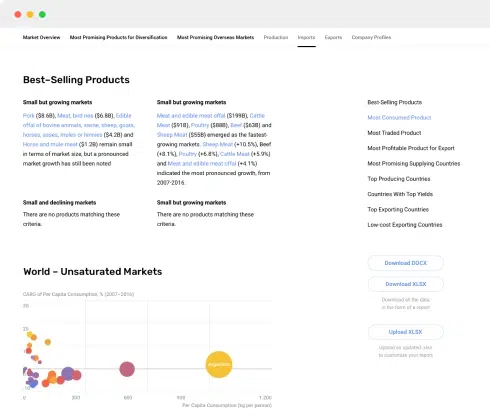

4. MOST PROMISING PRODUCTS FOR DIVERSIFICATION

Finding New Products to Diversify Your Business

- TOP PRODUCTS TO DIVERSIFY YOUR BUSINESS

- BEST-SELLING PRODUCTS

- MOST CONSUMED PRODUCTS

- MOST TRADED PRODUCTS

- MOST PROFITABLE PRODUCTS FOR EXPORTS

5. MOST PROMISING SUPPLYING COUNTRIES

Choosing the Best Countries to Establish Your Sustainable Supply Chain

- TOP COUNTRIES TO SOURCE YOUR PRODUCT

- TOP PRODUCING COUNTRIES

- TOP EXPORTING COUNTRIES

- LOW-COST EXPORTING COUNTRIES

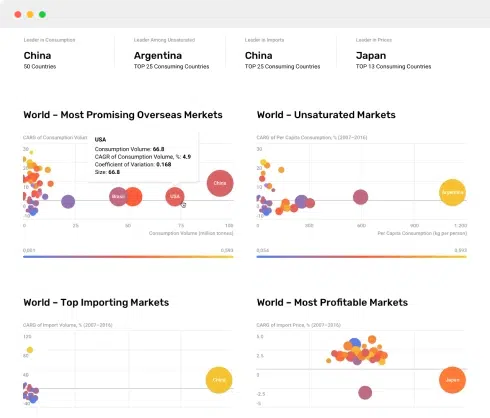

6. MOST PROMISING OVERSEAS MARKETS

Choosing the Best Countries to Boost Your Export

- TOP OVERSEAS MARKETS FOR EXPORTING YOUR PRODUCT

- TOP CONSUMING MARKETS

- UNSATURATED MARKETS

- TOP IMPORTING MARKETS

- MOST PROFITABLE MARKETS

7. PRODUCTION

The Latest Trends and Insights into The Industry

- PRODUCTION VOLUME AND VALUE: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

8. IMPORTS

The Largest Import Supplying Countries

- IMPORTS: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- IMPORTS BY COUNTRY: HISTORICAL DATA (2012–2024)

- IMPORT PRICES BY COUNTRY: HISTORICAL DATA (2012–2024)

9. EXPORTS

The Largest Destinations for Exports

- EXPORTS: HISTORICAL DATA (2012–2024) AND FORECAST (2025–2035)

- EXPORTS BY COUNTRY: HISTORICAL DATA (2012–2024)

- EXPORT PRICES BY COUNTRY: HISTORICAL DATA (2012–2024)

10. PROFILES OF MAJOR PRODUCERS

The Largest Producers on The Market and Their Profiles

LIST OF TABLES

- Key Findings In 2024

- Market Volume, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Market Value: Historical Data (2012–2024) and Forecast (2025–2035)

- Per Capita Consumption: Historical Data (2012–2024) and Forecast (2025–2035)

- Imports, In Physical Terms, By Country, 2012–2024

- Imports, In Value Terms, By Country, 2012–2024

- Import Prices, By Country, 2012–2024

- Exports, In Physical Terms, By Country, 2012–2024

- Exports, In Value Terms, By Country, 2012–2024

- Export Prices, By Country, 2012–2024

LIST OF FIGURES

- Market Volume, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Market Value: Historical Data (2012–2024) and Forecast (2025–2035)

- Market Structure – Domestic Supply vs. Imports, in Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Market Structure – Domestic Supply vs. Imports, in Value Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Trade Balance, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Trade Balance, In Value Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Per Capita Consumption: Historical Data (2012–2024) and Forecast (2025–2035)

- Market Volume Forecast to 2035

- Market Value Forecast to 2035

- Market Size and Growth, By Product

- Average Per Capita Consumption, By Product

- Exports and Growth, By Product

- Export Prices and Growth, By Product

- Production Volume and Growth

- Exports and Growth

- Export Prices and Growth

- Market Size and Growth

- Per Capita Consumption

- Imports and Growth

- Import Prices

- Production, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Production, In Value Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Imports, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Imports, In Value Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Imports, In Physical Terms, By Country, 2024

- Imports, In Physical Terms, By Country, 2012–2024

- Imports, In Value Terms, By Country, 2012–2024

- Import Prices, By Country, 2012–2024

- Exports, In Physical Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Exports, In Value Terms: Historical Data (2012–2024) and Forecast (2025–2035)

- Exports, In Physical Terms, By Country, 2024

- Exports, In Physical Terms, By Country, 2012–2024

- Exports, In Value Terms, By Country, 2012–2024

- Export Prices, By Country, 2012–2024